How Solana is Capturing Capital From Outside Crypto

Tl;dr:

This has been a brutal year for crypto. Prices are down across the board, volume thinned out, and sentiment has sat near multi-year lows for months. Solana took the price hit like everyone else, with SOL falling hard from its January high. But the fundamentals went the other way. Solana held its lead in spot trading through the entire drawdown, and the capital on it stayed put rather than chasing the next hot chain.

What changed underneath was the source of the capital. Instead of just onchain trading activity, Solana started pulling in real outside capital from traditional finance. Tokenized equities, perpetuals, prediction markets, and bridged assets all stopped being side experiments and turned into steady, repeat volume.

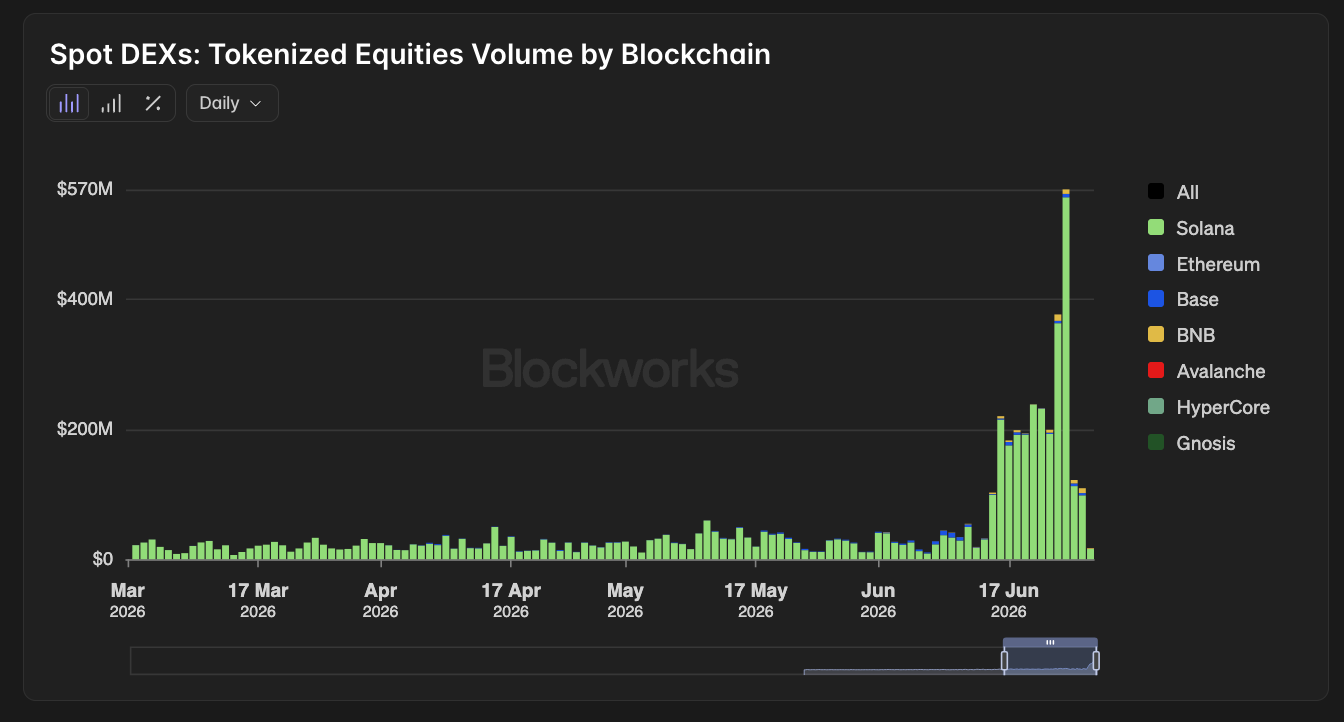

Tokenized stocks are the clearest example. A year ago, they had almost no volume, and now they move hundreds of millions in a day.

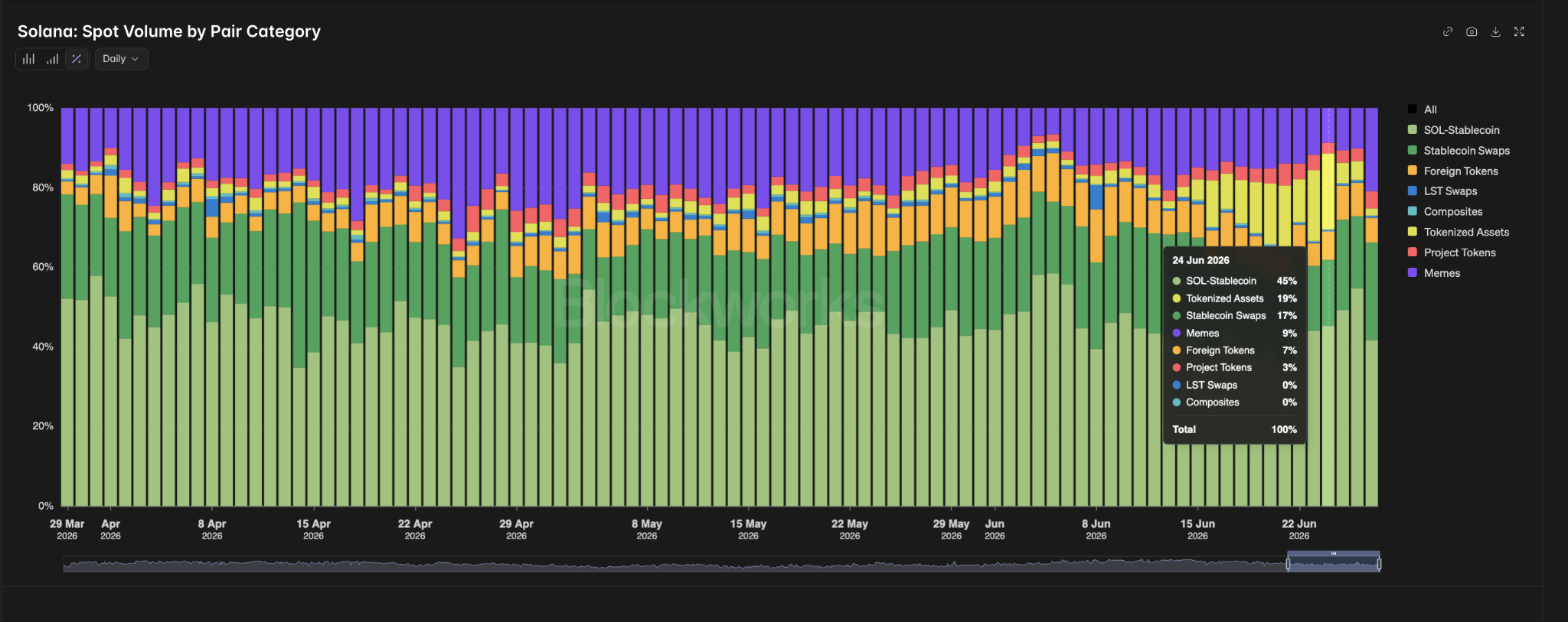

Tokenized equities volume on Solana hits an all-time high

On June 25, daily tokenized equity volume on Solana surpassed $553M, setting a new all-time high.

Solana settled around $871M of tokenized equities in May 2026, against roughly $895M across every chain combined. Base was the only other network above a million, at about $22M. Tokenized stocks are effectively a Solana product right now, not a multi-chain one.

Solana's own trading shows the shift too. On June 24, tokenized assets accounted for 19% of spot volume while memes fell to 9%. Solana made its retail name on memecoins, and it is now moving more equity than degen tokens on a given day.

Much of the recent surge traces to SPCX, the tokenized SpaceX stock Backpack launched on Solana the day SpaceX listed on Nasdaq, which cleared over $470M in its first week. The institutional pull this cycle is tokenized equities.

Source: https://x.com/fintechfrank/status/2071288187368964566?s=20

Why tokenized stocks are growing fastest on Solana

Tokenized equities are barely a year old on Solana, and the climb from almost no volume to half-billion-dollar trading days is one of the fastest any onchain category has run.

A tokenized stock is a token that tracks a real share one-to-one, with the underlying equity held by a regulated custodian, so it is a claim on an actual share rather than a synthetic bet on the price. Backed launched the first real version on Solana in mid-2025, a set called xStocks covering US names like Apple, Tesla, and Nvidia.

Living onchain gives the tokens two things the shares never had: they trade 24/7 instead of only at market hours, and they settle in seconds. The product went live through Kraken and Bybit and plugged into Solana DeFi, with liquidity on Raydium, routing through Jupiter, and collateral support on Kamino, so a holder can trade, swap, or borrow against the token without it leaving the chain.

The built-in numbers.

- H2 2025, the category's first six months, did $775M in total volume from a near-standstill.

- H1 2026 cleared roughly $4.9B, more than six times that, with monthly volume rising from $228M in January to about $2B in June.

- Market cap, the total value of tokenized stocks held onchain, grew about 3.5x across 2026, from $152.5M to $539M. Volume is how much trades, market cap is how much is held, and both rising together means new money is staying, not just passing through.

- On June 25, Solana settled $553M of tokenized equities in a single day, a new all-time high.

Who is building it. The established issuers compete in three different ways:

- xStocksFi is the size leader, holding 92% of tokenized-stock market cap, about $497M, and 62% of H1 2026 volume. It is the venue most of the money trades through.

- OndoFinance arrived in January and leads on breadth, with 438 tokenized stocks live. It competes on selection, listing far more tickers than anyone else.

- PreStocks is the velocity play. On about $16M of market cap it did $1.2B in volume, so its tokens turn over far faster than the rest. The reason is its niche: pre-IPO exposure to companies like SpaceX, OpenAI, and Anduril that have no public-market equivalent, where onchain is the only place retail can get in.

What drove the June breakout. The spike that took the category to its all-time high came from a newer model: tokenizing a company right as a market event puts it in the headlines. Backpack Securities ran it first with SPCX, the tokenized SpaceX stock, launched through the Sunrise listing gateway on the same day SpaceX hit Nasdaq. It cleared over $470M in its first week, the most of any tokenized SpaceX version, and unlike most of these tokens it can be redeemed for the actual underlying shares.

The playbook repeated days later with Micron (MU), brought onchain right before its quarterly earnings. Sunrise is the piece that makes this work, coordinating each new listing across Solana wallets, DEXs, and liquidity pools so a brand-new token trades with real depth from the first minute. A company now gets an onchain market the moment it has a public one.

Source: @birdeye_data

Beyond tokenized stocks: stablecoins, payments, and RWAs on Solana

Tokenized stocks are the loudest example, but they are one lane of a much wider move. Outside money is arriving across the whole financial stack on Solana, and most of it is not crypto-native:

- Stablecoins. Stablecoin supply on Solana held around $15.8B through the downturn (rwa.xyz). The new issuers are the tell: Western Union's USDPT, a regulated dollar issued through Anchorage, a federally chartered crypto bank, and SoFi's SoFiUSD, the first stablecoin from a US nationally chartered bank, opened to its roughly 15 million members. World Liberty's USD1 scaled past $1B and Ethena's USDe reached about $547M alongside them.

- Payments. Onchain payment volume rose 87% year-over-year and card payments did 5x more than the year before, pushing Solana's card-payment share from 5.43% to 10.1%. Visa now settles US card obligations in USDC on Solana, and Mastercard added stablecoin settlement across its network.

- Tokenized funds and credit. Real-world assets onchain have climbed toward $3B (@rwa_xyz), with BlackRock, Apollo, Janus Henderson, Securitize, and Ondo bringing traditional funds and credit products onto the network.

- Capital from other chains. Bridged BTC and ETH shrank on Solana while foreign L1 assets surged, led by HYPE, which did $3.1B in cumulative volume with 95% of it this year and on June 4 traded more spot volume on Solana than every centralized exchange combined.

. - New onchain markets. Perpetuals and prediction markets stopped being experiments too. Solana hosts more prediction-market platforms than any chain, 37 against Polygon's 13, and its perps volume grew 57% year-over-year, well ahead of Hyperliquid's growth rate.

Equities, regulated dollars, card settlement, tokenized funds, and bridged capital are all landing in the same place, which is what makes this a shift in where money lives rather than a single hot product.

How Solana's upgrades made it ready for institutional capital

Solana did not pull in this capital by being cheap. It fixed the specific things that kept professional money out, and each fix answered a complaint institutions had made for years.

Performance and cost came first. Bigger blocks and a token-program rewrite that cut transfer costs by about 98% gave the network room to run at scale. Predictability matters as much as the level: on most chains congestion anywhere lifts fees everywhere, but Solana prices it per account, so a frenzy on one token does not raise costs for a fund settling tokenized assets three pools over.

Reliability was the other long-standing blocker. The network ran on a single validator client, so one bug could threaten the whole chain, and that outage history kept desks on the sidelines. Firedancer, a fully independent second client live on mainnet since late 2025, removes that single point of failure.

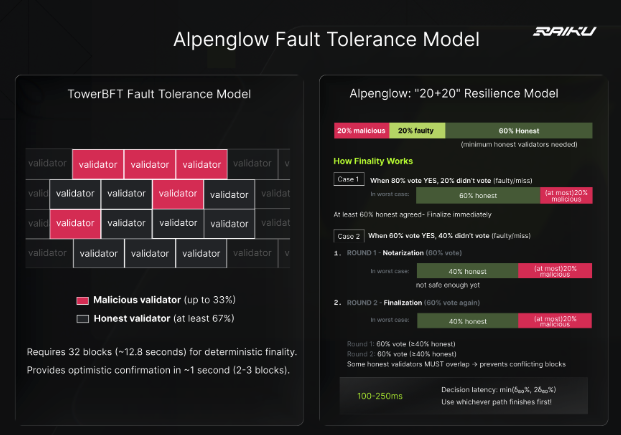

Settlement is the next piece, still in progress. Full finality takes about 13 seconds today, and a market maker prices every second its capital sits exposed. Alpenglow, now rolling out, cuts that toward 100–150 milliseconds.

Together the live upgrades cleared most of the ground, and the proof shows up on SOL-USDC, where a trade costs about 1.22 basis points onchain against 8.33 on Binance's best tier. But clearing the ground is not the same as finishing the job. Every one of these fixes makes a transaction cheaper, safer, or faster on average, and averages are exactly what the biggest capital cannot rely on. The trade that matters is not the average one. It is the redemption that has to settle at 4pm, the liquidation that has to fire the second a position breaks, the cancel that has to land before the market moves. None of the upgrades above can promise that specific transaction lands at that specific moment, and until something can, the largest money stays cautious.

The missing piece for institutional Solana: guaranteed execution

For serious money, timing is the whole game. And the need for it splits across two kinds of capital that want certainty for opposite reasons:

- Fast money (market makers, trading desks) cares about speed and outcome. It fires thousands of quotes and cancels a day, and it needs to know an order or a cancellation lands in time. The moment it can't trust that, a faster player picks off its stale quote.

- Slow money (funds, credit and money markets) might send a handful of transactions a day, and for it certainty has nothing to do with speed. It is about executing the one thing that has to happen when everything else is going wrong, the redemption, the settlement, the liquidation, without that single transaction failing at the worst possible moment.

Both hit the same wall. The transactions that matter most are the ones that cannot wait, and each fails if it lands a few slots late or gets dropped when the network is busy:

- A fund settling redemptions at a set window.

- An oracle repricing collateral in the middle of a selloff.

- A liquidation that has to fire the instant a position breaks.

On a chain where you pay for blockspace and hope to make the next block, that risk never fully goes away, and unpriced risk is what keeps large capital out. It is the same calculation a desk makes before touching any new venue: the returns might be real, but if proving it means absorbing the risk that the venue fails when it counts, most run the math and stay home.

This is the layer traditional finance spent decades engineering away. A professional desk pays for infrastructure precisely so it knows, before it commits, what it will get: how fast an order lands, what it costs, whether it can cancel in time. Onchain skipped that layer. The upgrades above rebuilt most of it, fast settlement, clean data, low and stable costs, but they stop short of the last guarantee: that a specific transaction lands in a specific block at a known time.

That guarantee is the problem Raiku works on. Validators set aside part of their blockspace, and an application reserves it ahead instead of bidding into the next block and hoping. The two products map onto the two kinds of failure above:

- Ahead-of-time (AOT) reservations handle anything scheduled. A fund settling redemptions at a set window or an oracle that has to reprice on time locks its slot in advance, so the transaction lands on schedule no matter how congested the chain gets.

- Just-in-time (JIT) execution handles anything that can't wait. A liquidation that has to fire the instant a position breaks claims the next available slot, shielded from being dropped under load.

A lending market will only accept a tokenized stock as collateral if it trusts the liquidation will fire when it must; a fund will only settle onchain if it knows its transaction lands in its window. That certainty is the line between a chain you can trade on and one an institution can settle on, and it is the last piece of the foundation the rest of this capital is being built on.