How to choose the right Solana LST: A data study of 200+ Liquid Staking Tokens

We analyzed 200+ Solana LSTs. Here's what we found.

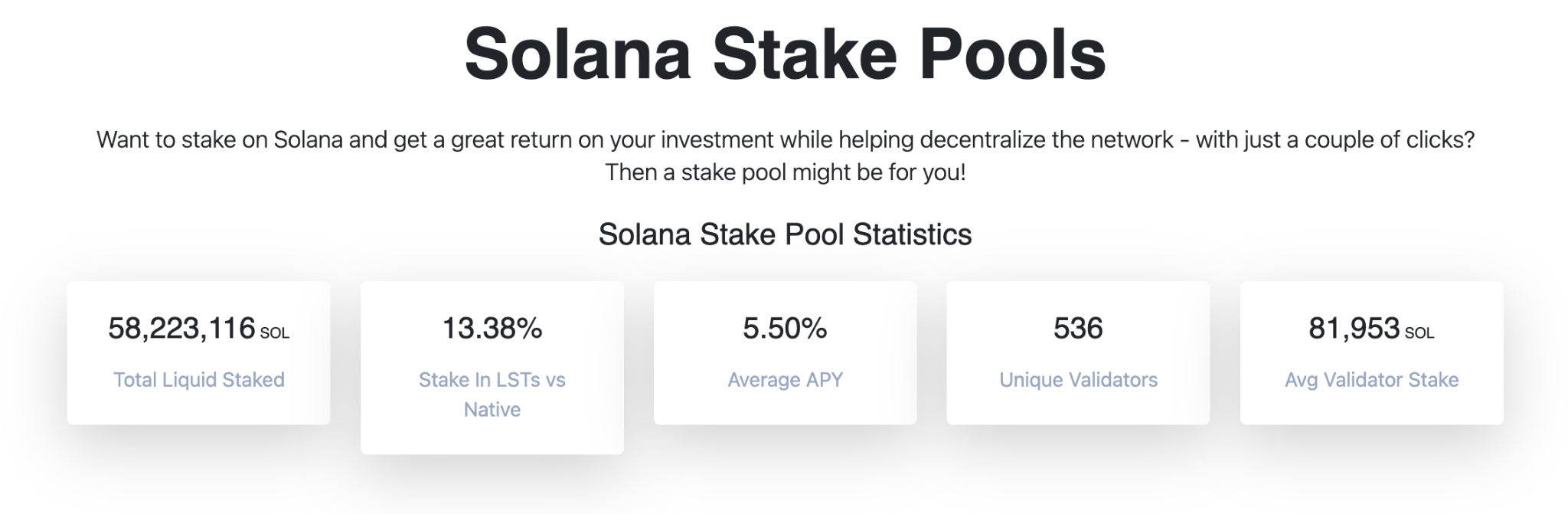

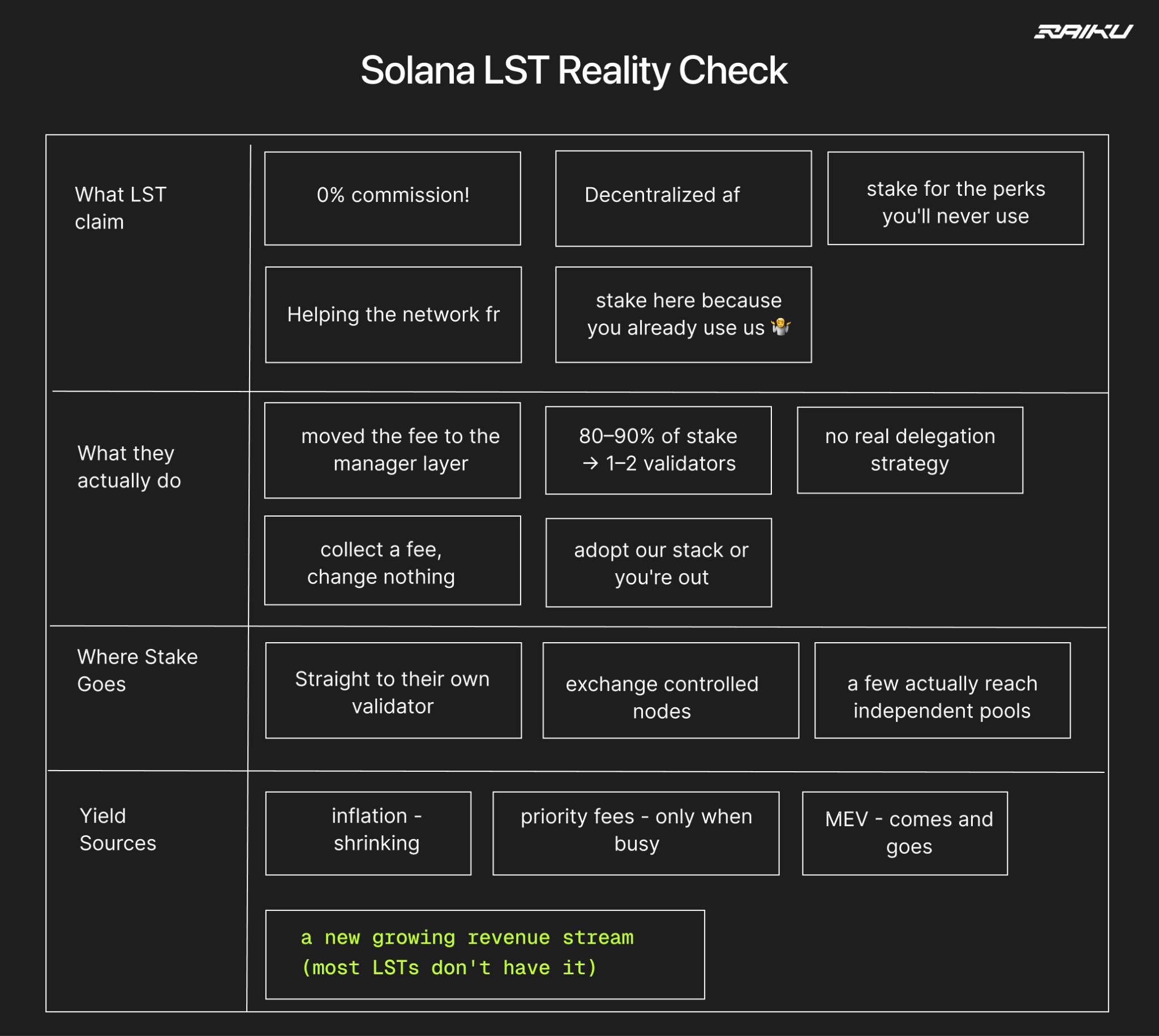

TL;DR: Of the 206 LSTs on Solana, only a few dozen hold meaningful stake, and the live ones nearly all pay the same yield. So, yield can't be how you choose. What separates one LST from another is what it does with the stake it controls: most park it on captive validators and collect a fee, a few use it to push validators toward real network work or explore meaningful new revenue sources beyond the traditional ones.

These tokens hold about 58.5M SOL between them (data from Solana Compass), and we studied all of them, looking at TVL, delegation patterns, validator distribution, fee structures, and what each does with the stake it controls.

https://solanacompass.com/stake-pools

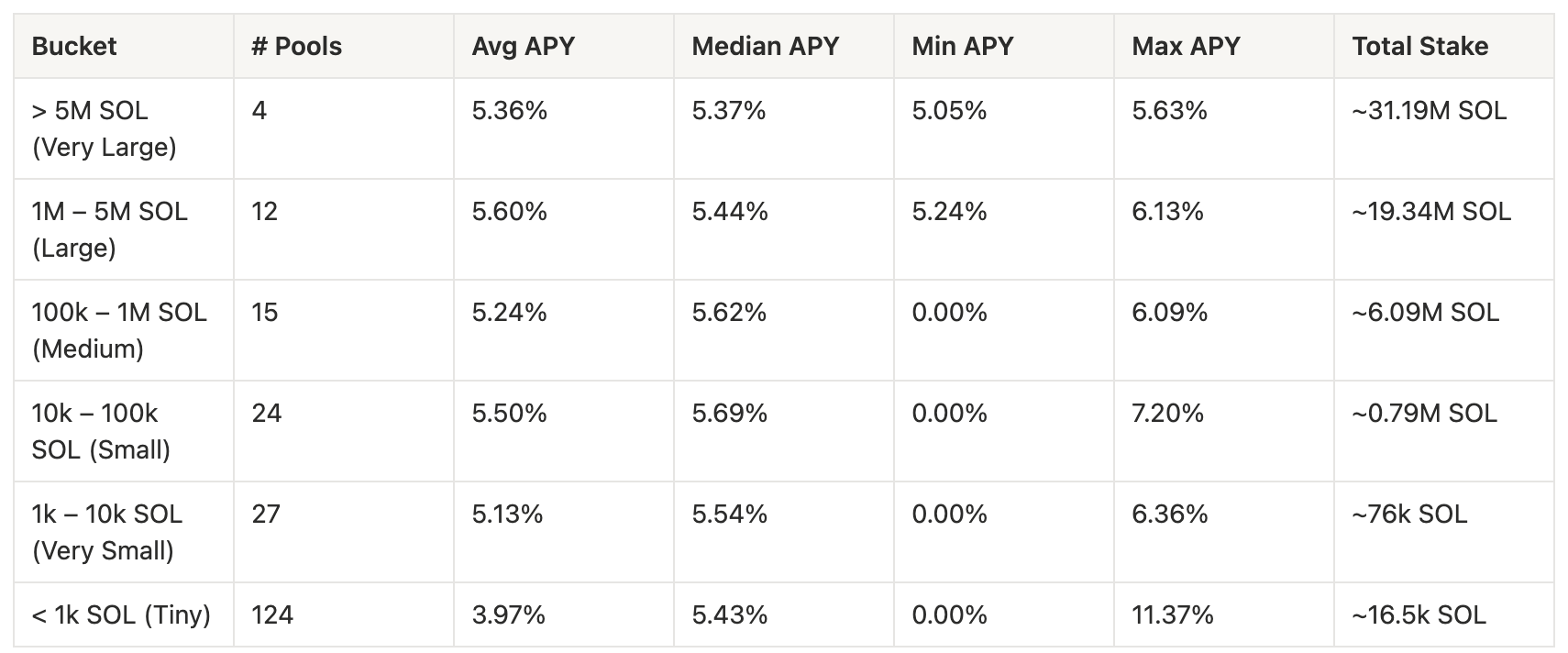

The market is quite concentrated:

- 4 tokens hold more than 5M SOL each. Together, that's 53% of the entire market.

- 12 more hold between 1M and 5M, another 33%.

- Below that, around 20 tokens hold between 100K and 1M.

- Everything else, roughly 170 tokens, holds barely 1% combined. Dead pools, abandoned projects, vanity launches, plenty with less than 10 SOL.

Here's where most people go wrong when picking between them.

Common mistakes people make when choosing a Solana LST

Most stakers pick an LST on one of two signals: the yield or a name they recognize.

#1: Choosing LST just based on APY

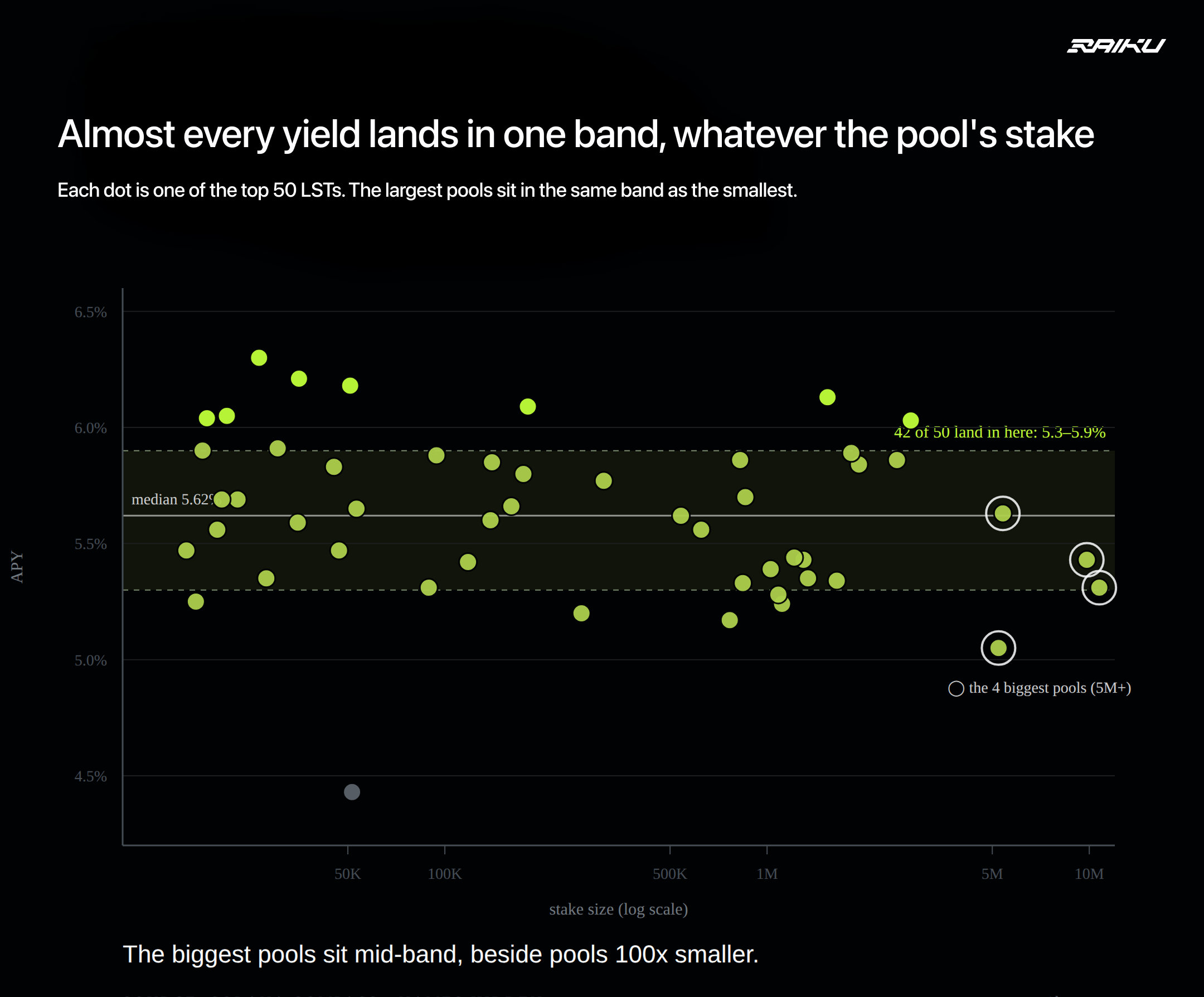

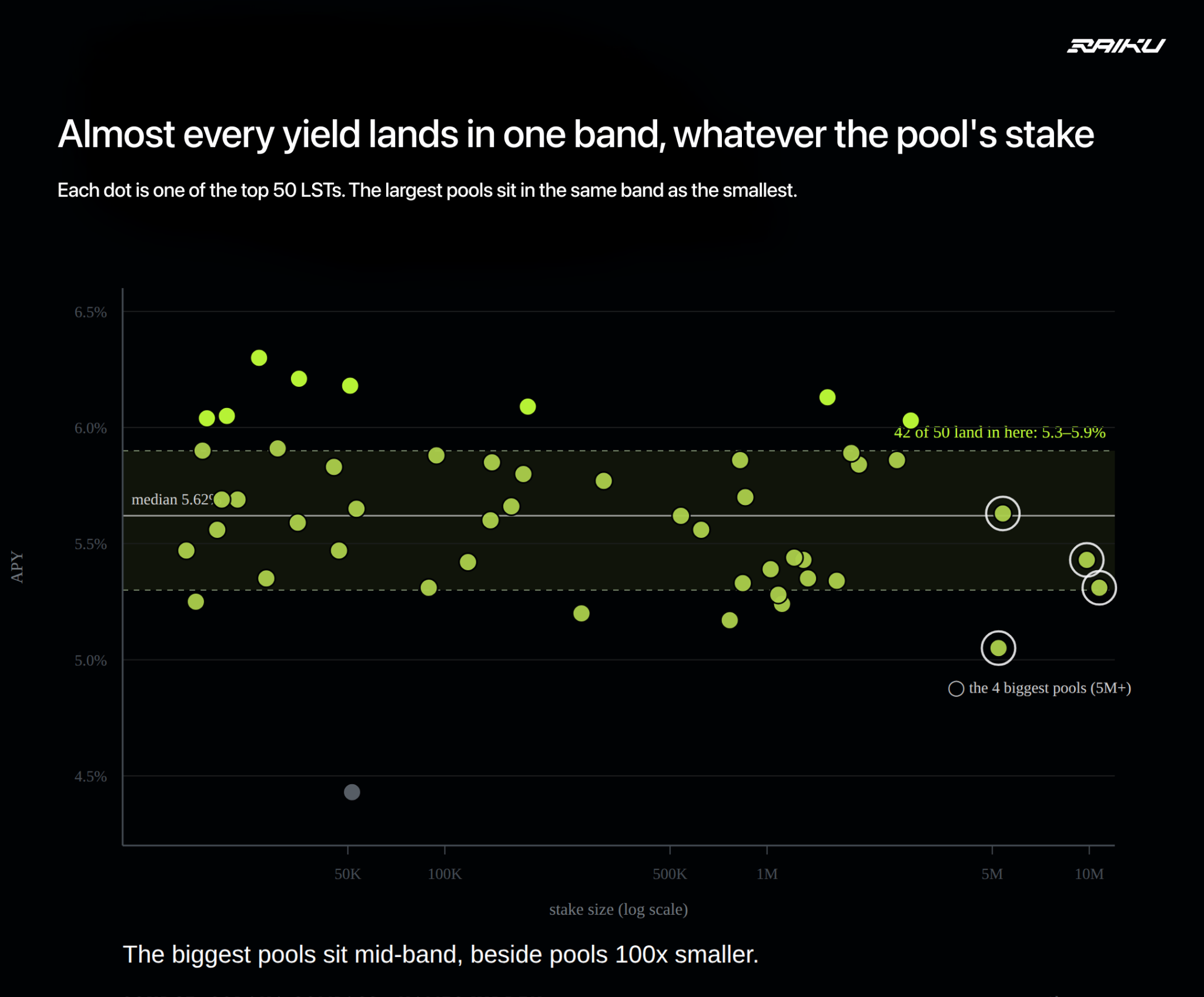

When choosing an LST, the first thing most people look at is APY, and for many, it's the only thing. They sort the list and pick the highest number. The yield is nearly flat across the market. The median APY barely moves across the whole market. Bucket every LST by size and it stays flat from the largest pools to the smallest, with the live ones sitting between roughly 5.3% and 5.9%:

So what does the top of the table win you? Maybe half a percent over a typical pool. On 100 SOL staked, that comes to about half a SOL a year, before fees, liquidity, or risk enter the picture. The hunt for the highest number pays out a rounding error.

The extreme cells aren't real returns:

- The high Max figures (7.20%, 11.37%) come from the Small and Tiny buckets, where a pool holds a few hundred SOL or less and one reward event distorts the annualized rate

- The 0.00% Min figures are dead pools, and they drag the Tiny bucket's average down to 3.97% while its median holds at a normal 5.43%

Once a pool holds real stake, its APY settles back into the same band as everyone else.

Why APY shouldn't be your deciding factor

A few named pools do pay a real premium that holds up over time. The catch shows up when you check how each one earns it. There are only a few ways an LST pushes its APY above the pack:

- Subsidy. The protocol covers validator commissions out of its own treasury to lift the number. The yield comes from the protocol's pocket, not the network, and it stops the day the protocol stops paying.

- Owning the validator. Stake goes to one validator the issuer runs, at 0% commission. The extra yield is just one fewer cut taken along the way, and that cut usually comes back as a manager fee or an exit fee. Everything sits on a single validator.

- Priority fees. Some pools pass transaction priority fees through to holders. The amount is small and swings with how busy the network is, and any validator can do the same.

- Lower fees. A pool can charge less. The headline improves while the pool does nothing more, and the fee can go back up whenever the issuer decides.

Two pools earn the premium a different way:

- MEV. JitoSOL captures value from transaction ordering through the Jito client, across hundreds of validators. The revenue is real and comes from the network itself. It also swings with the market, high when things are volatile and thin when they're quiet, and the delegation behind it has become contested.

- Validator competition. mSOL makes validators bid part of their commission back to holders to win stake, across 100+ validators. It pays a little less than the MEV pools, because Marinade won't force validators onto the centralizing client choice.

The pattern holds across the list. The pools paying above-market APY are mostly doing it through a subsidy, a single captive validator, or a temporary fee cut:

- The highest-yielding pools all run on one validator (dSOL, PSOL, fwdSOL)

- dzSOL, spread across 287 validators, sits near the bottom of the APY column

So APY can't be how you choose

Yield is your return, so it matters. But the real pools all land within a percentage point of each other, and a number that barely moves can't be what tells them apart. The variation that does exist usually tracks how the pool is built, not how good it is, and it often points toward the more centralized option. So if two LSTs both pay you 5.5%, what separates them? Not the APY. What the pool does with the stake, and where the yield comes from.

#2: Choosing a Solana LST by brand or convenience

Most SOL doesn't get staked through an LST after someone compares the options. It gets staked because the option was already in front of the holder. SOL sitting on Binance gets staked through Binance's button. SOL in Phantom gets staked through the option next to the balance. The same holds for Jupiter and Drift users. The app the holder has already opened makes the choice.

bnSOL shows how far that goes. It is the largest liquid staking token in the market, and Binance built that position on purpose rather than earning it on staking performance. The growth came from four things working together:

- A captive base of users already holding idle SOL on the exchange, reachable through staking, spot buys, Auto-Invest, and Convert

- A boosted launch APR running through the end of 2024 to pull early deposits in

- Super Stake, a recurring program paying holders airdrops of other tokens (PIXEL, OM, PEPE) on top of the base yield

- Fast DeFi integration across Kamino, Drift, Raydium, Meteora, Solayer and others, so the token was useful everywhere a Binance user might go

It crossed $1B in TVL and roughly 10% of the entire LST market this way, while charging one of the highest fee cuts in the category and routing every lamport to Binance-run validators.

None of that is staking performance. Binance paid to acquire the deposits with boosted yield and a rotating airdrop machine, then made the token sticky by wiring it into Solana DeFi. The validators behind it were chosen before launch and earn the stake regardless of what they do. bnSOL reached the top of the market without ever using its delegation for anything beyond Binance's own balance sheet.

Every large brand LST runs a version of this:

- bnSOL converts idle SOL already sitting on Binance

- JupSOL grew on Jupiter's user base, large enough that Jupiter became one of Solana's biggest validators

- PSOL, bbSOL, gtSOL, and dSOL each convert the users inside their own wallet, exchange, or app

The platform is the product in every case, and the token is a feature added to it. The stake came from distribution and incentives, not from the pool being good at the one job an LST has.

A holder who picks this way never reaches the question that decides whether an LST is any good: what happens to the SOL after the pool receives it, who runs the validator behind the token, and whether the stake does anything beyond earning the issuer a fee. A familiar name signals convenience. Convenience says nothing about how the stake is used, and how the stake is used is what separates one LST from another.

Trusting a protocol you already use to handle your stake is fine, that's the point of an LST. The mistake is doing it without knowing what happens to the stake once the protocol has it. A familiar name tells you the token is convenient, nothing more. Which is the third mistake.

#3: Ignoring what the LST does with your staked SOL

The first two mistakes are about how you pick: by yield or by name. This one is what you skip: the stake keeps working after the pool receives it, and what it does there is the only thing separating two pools that both pay 5.5%.

An LST does three things with the SOL it collects.

- Pools stake. Many depositors' SOL becomes one large position. That concentration is what creates leverage over validators.

- Chooses validators. The pool decides where the stake goes, not you. This is where LSTs split in two: stake pools spread deposits across many validators; validator LSTs route everything to a single validator the issuer controls. One is a delegation strategy; the other is one destination with a token wrapped around it.

- Sets conditions. The pool can demand things for the stake, a performance bar, specific software, a connection to specific infrastructure. Validators that want the delegation have to meet the terms.

Together, that's a routing system for stake. And on Solana, a validator's stake decides its influence in consensus, how often it produces blocks, and whether it earns enough to survive. Where the stake goes shapes the validator set.

So an LST has a second job beyond paying yield: deciding which validators gain power, which stay alive, and what they must do to keep the stake. The first job is why you buy an LST. The second is what makes one good or bad.

Most LSTs ignore that second job. Take bnSOL again, every lamport routed to Binance's own validators, nothing required of them in return. We saw how it grew; the point here is what happens after: 11M SOL of delegation power, the one scarce thing an LST holds, does nothing with it. It secures the chain at the baseline and stops.

That's the catch: a pool parking its stake on captive validators and one using it to push the network forward can show you the same APY. The yield never tells you which you're holding. Only what's underneath does.

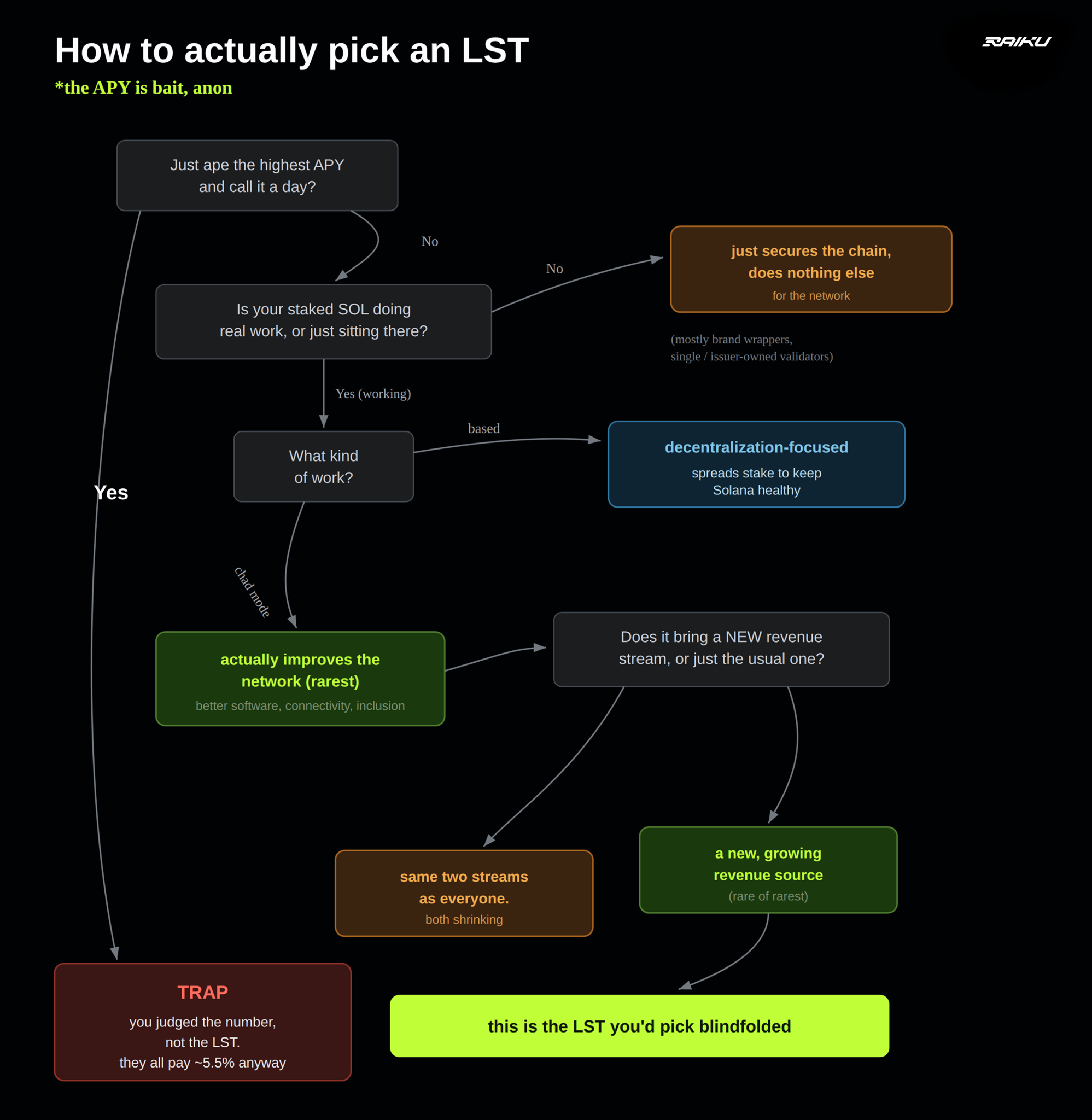

How to choose a good Solana LST

Good LSTs share two traits, and the first is about the validators.

#1: Choose an LST that puts validators to work

For an LST to be worth holding long-term, its stake should be tied to real work, doing something that improves Solana as a network, rather than simply sitting on a validator and collecting a fee.

This work happens at the validator level, because that’s where delegation actually flows. An LST decides where stake goes, and that decision influences what software validators run, whether a transaction is guaranteed to land or can get dropped, how fast blocks propagate, how transactions are ordered, and how concentrated stake becomes. These are some of Solana’s hardest remaining challenges.

As Solana grows, these problems become more pressing. Validators that actively solve them will pull ahead, while those that don’t will fall behind. This creates a natural divergence:

- Work-first LSTs direct stake toward validators doing meaningful work. As the network demands more from validators, these LSTs become more relevant and can grow even if they start smaller.

- Brand wrappers, on the other hand, usually park stake on captive validators that were set up mainly to collect fees. Their growth is limited to the size of their existing user base, and they have little ability to improve the validators behind them.

In short, an LST is only as strong as the validators it funds. When those validators improve, the LST tied to them improves too. When they stagnate, the LST stagnates with them.A few clear examples of this approach:

1. JitoSOL: stake tied to MEV adoption

JitoSOL is the original. It routed stake only to validators running Jito's MEV software; validators ran it to qualify, and within about two years, most of the network had adopted it. That adoption is why Solana has a functioning MEV system: before it, bots spammed the network and validators captured almost none of the value. Attaching a stake to the software made running it a profitable choice.

The same mechanism now draws pushback. Jito is tying JitoSOL's delegation to BAM, its new block-building stack, and removing validators that won't run it. Qualifying requires a 0% commission, which validators argue on Jito's own forum pushes out everyone except the largest operators. The mechanism that once rewarded validators for adopting better software now pressures them, which shows the pressure cuts both ways.

@ValidBlocks

2. dzSOL: stake tied to network connectivity

dzSOL applies the model to networking. DoubleZero runs a private fiber backbone for validators, low-latency links between data centers instead of consensus traffic crossing the public internet, and dzSOL delegates only to validators connected to it. Today that buys a performance edge, fewer skipped slots and faster propagation. The larger reason is Solana's MCP upgrade: once it ships, validators will send blocks to each other in patterns the public internet was not built for, and the ones dzSOL is pulling onto fiber now are the ones that will still function afterward.

3. Marinade: stake tied to decentralization

Marinade Finance runs a softer version. Instead of pushing one piece of software, it uses delegation to keep the validator set spread out, penalizing validators that grow too large and scoring the rest on geographic and data-center diversity. Different goal, same move: spending stake to shape validator behavior instead of parking it.

4. rkuSOL: stake tied to guaranteed blockspace

rkuSOL is the newest to run the model. Raiku sells guaranteed transaction inclusion through its auctions, where buyers reserve space in upcoming blocks ahead of time, and rkuSOL delegates only to validators running Raiku's software to supply it. That ties the stake to a kind of work none of the others touch: making block inclusion something an application can pay for and count on. It is early, around 89,000 SOL today against the millions the names above hold, but the mechanism is the same one that built JitoSOL.

What connects all four is delegation spent as infrastructure investment. These LSTs use pooled stake to fund and force work the network needs, better software, better connectivity, wider decentralization, guaranteed inclusion, work that would not happen otherwise. Validators reorganize to qualify because the stake is worth more than the cost of qualifying.

#2 Choose an LST with a sustainable validator revenue source

Most LSTs on Solana currently generate yield from the same two sources: network inflation and MEV/priority fees.

Inflation is on a scheduled decline toward a 1.5% floor, while MEV and priority fees are real but highly cyclical, they depend heavily on network activity and market conditions. As a result, almost all LSTs end up offering very similar yields. When everyone is drawing from the same limited and increasingly unpredictable pool of revenue, there is little room for real differentiation.

This is why the search for new revenue sources matters. In a market where most LSTs are competing over slices of the same shrinking pie, the ones that can access genuinely new sources of revenue have a structural advantage. It’s not just about earning slightly more today, it’s about whether an LST can continue creating value as inflation continues to decline and MEV remains volatile.

The only meaningful way to break out of the current narrow yield band is by giving validators access to revenue streams that didn’t exist before. This is rare, because building a new, sustainable revenue model for validators is significantly harder than simply routing stake differently or offering lower fees.

So far, MEV has been the only major addition to the staking yield base in recent years. Since then, very few LSTs have managed to introduce something structurally new.

One early example is rkuSOL. Its validators participate in blockspace auctions, where they offer to reserve space in upcoming blocks for buyers who pay in advance. This creates a new revenue stream for validators that is:

- Priced before the block is produced

- Less dependent on network congestion or activity

- Potentially scalable with actual demand for blockspace

Instead of waiting for transactions to arrive and compete for space, validators can generate revenue by selling reserved capacity upfront. This revenue can then flow back to stakers through the LST.While it is still very early and only a few weeks of data is available, rkuSOL represents an attempt to expand the total revenue available to validators and stakers, rather than competing over the same existing sources.The broader point remains: as inflation continues to decrease, LSTs that can access new forms of validator revenue are better positioned to create lasting differentiation compared to those that rely entirely on the traditional two streams.

Conclusion

Choosing an LST is no longer just a decision about yield. It’s a decision about where your delegation power goes and what kind of network it supports.

Most LSTs today still operate in the old model, they collect stake, park it on a few validators, and collect a fee. A smaller group is beginning to use that same power more deliberately: to push validators toward better software, stronger infrastructure, wider decentralization, or entirely new revenue models.

As inflation continues to decline and Solana scales, the difference between these two approaches will become more visible. The LSTs that treat stake as passive capital will have fewer ways to stand out. The ones that treat it as active infrastructure will have more room to create real, lasting value.

In the end, your choice of LST is a quiet but meaningful vote on what Solana becomes.

About Raiku and rkuSOL

Raiku is blockspace infrastructure on Solana, built to make transaction execution reliable enough for institutions and high-volume applications. It turns blockspace from an unpredictable commodity into a guaranteed, programmable resource through two markets: ahead-of-time reservations, where applications lock in compute for upcoming blocks in advance, and just-in-time execution for transactions that need to land in the current slot.

This is what creates the new revenue line. Validators already securing Solana can offer guaranteed inclusion as an additional service, earning from blockspace reservations on top of their existing staking and MEV income, without giving up either.

rkuSOL is Raiku's liquid staking token. It delegates stake to validators running Raiku's software, so the yield is tied to that blockspace revenue rather than to inflation alone. As demand for guaranteed execution grows, the revenue feeding rkuSOL grows with it, a source that doesn't depend on Solana's inflation schedule or on volatile MEV.

Read more: