rkuSOL just entered the Solana LST top 30 within its first week. Here's what every LST in that group actually does.

Less than a week after launch, rkuSOL entered the top 30 Solana LSTs by Sanctum's tracker. A week in this is a big achievement and to celebrate the milestone we’re taking a look at the rest of the list and asking what every LST in it is actually for.

Liquid staking on Solana is now a roughly $8 billion market spread across more than 200 tokens, but the top 30 hold around 94% of all liquid-staked SOL. The rest are mostly inactive pools, dormant projects, or vanity launches, which means the meaningful market is essentially this group of 30. Looking at it closely, the differences between them are bigger than the headline APYs suggest.

This piece walks through the ten most distinctive LSTs in the top 30, what they're for, what they earn yield from, and what they actually do with the delegation power that comes with the stake they hold. rkuSOL sits in there too, and the framing makes more sense once the rest of the picture is clear.

The four groups inside the top 30

Before some individual breakdowns, it's worth being clear about how to think about LSTs as a category. The top 30 mostly fall into four groups:

Group 1, work-first LSTs. These tie their delegation to validators doing specific infrastructure work that the network depends on. JitoSOL pulled validators onto the MEV stack. dzSOL pulls them onto DoubleZero's fiber backbone. The defining feature is that the work comes first and the LST exists to align stake with it.

Group 2, decentralisation-pressure LSTs. These don't run infrastructure directly but use their delegation to fight stake concentration and push the validator set wider. Marinade is the largest example. Layer 33 (Indie Soul) is built around supporting independent validators specifically.

Group 3, ecosystem and infrastructure LSTs. Real work that helps the ecosystem but operates at a layer different from validator behaviour. Sanctum sits here, as does Rakurai (a high-performance validator client). The work is meaningful, but it's infrastructure for LSTs and applications rather than infrastructure for Solana itself.

Group 4, brand wrappers. Exchange convenience products and app-tied loyalty tokens. They route stake to validators they control, charge fees, and pass yield through. The category includes the largest LST in the market.

rkuSOL sits in its own corner of Group 1, as the first LST whose underlying yield includes contractually-paid blockspace revenue on top of staking and MEV. More on where it fits at the end.

Ten LSTs that actually tell you something about the market

JitoSOL

The LST that defined the ‘work-first’ model. JitoSOL only delegates to validators running the Jito client, which means stakers in JitoSOL get exposure to MEV revenue directly. Tens of millions of SOL across more than 300 validators. The current debate around it is BAM, Jito's new block-building stack, which is being tied to JitoSOL's delegation set in a way that's caused real pushback from smaller validators about whether the conditions push them out of the set. The original mechanism (delegation conditional on infrastructure adoption) is the template every work-first LST since has followed.

dzSOL

The cleanest current example of the work-first model. DoubleZero is building a private fiber backbone for Solana validators, with consensus-critical traffic running over dedicated low-latency links instead of the public internet. dzSOL delegates exclusively to validators connected to DoubleZero, with allocation weighted by how long they've been on the network. What makes it more than a niche infrastructure play is that Solana's upcoming MCP upgrade needs the kind of validator-to-validator traffic that DoubleZero's network is designed for, so the validators dzSOL is pulling onto the network now are the ones already positioned for that upgrade.

Marinade (mSOL)

The largest decentralisation-pressure LST. Marinade runs algorithmic delegation with explicit concentration penalties, where validators above a certain stake threshold become ineligible, and the algorithm scores the rest on yield, geographic distribution, and data centre diversity. The output is a stake distribution that actively avoids piling onto the validators most LSTs default to. Not the highest APY in the market, but the cleanest answer to the question of what an LST can do for network decentralisation at scale.

bnSOL

The largest LST in the market by some distance. Around 11M SOL routed almost entirely to one Binance-controlled validator, with four other validators on paper that exist mostly as decoration. bnSOL grew so large because Binance has hundreds of millions of users sitting on idle SOL, and wrapping that SOL into an LST keeps it on the exchange while earning yield. The product is exchange convenience at scale rather than anything that meaningfully contributes to Solana's infrastructure or decentralisation, and the fact that it's the largest LST in the market by some distance is worth thinking about as a market signal.

JupSOL

The clearest example of an app-tied loyalty LST. JupSOL exists to keep stake inside Jupiter's routing infrastructure and gives Jupiter users smoother in-app staking. Four validators on paper, but the vast majority of stake goes to Jupiter's own validator, with the others getting most of their stake from JupSOL itself. The actual product is the integration with Jupiter's main app, with the LST being more of an on-ramp to that experience, which is fine on its own terms but doesn't change anything about how Solana works underneath.

Layer 33 (Indie Soul)

A coalition of independent validators targeting a specific structural goal: getting 33% of total network stake on independent operators, the threshold above which no small group of large validators can compromise consensus. The whole product exists to fight centralisation at the network level. Smaller than the giants, but worth knowing about because it's the clearest example of an LST built around a single, falsifiable, public goal.

Sanctum (sctmSOL)

A category of one, really. Sanctum built the router, the shared liquidity layer, and the launch tooling that nearly every other validator LST on this list runs on top of. sctmSOL itself is part of that broader infrastructure layer rather than a product that does something specific for the Solana protocol. The work is genuinely important to the LST ecosystem (which is why so many LSTs sit on top of Sanctum's infrastructure), and rkuSOL is among the LSTs that benefits from it directly.

dSOL

Drift's LST, built so traders can use staked SOL as 101x perps margin without leaving Drift. Single validator. Significant stake. Useful if you happen to live inside Drift, less interesting if you don't. The product is really the perps integration with the LST providing the on-ramp, and not much is happening at the Solana network level as a result.

fwdSOL (Forward Industries)

The treasury LST category, and the most interesting corner case. Forward Industries holds around 7M SOL on its balance sheet, and fwdSOL exists primarily so the company can stake that position, borrow against the LST on Kamino at rates below the underlying yield, and run the spread on its own treasury. The retail wrapper is genuinely incidental to what fwdSOL is actually for. The product is the corporate treasury strategy, with the LST existing to enable it. Worth knowing about because it's an early example of treasury management as a real use case for crypto LSTs, and there are more publicly-listed companies likely to follow Forward's model.

rkuSOL

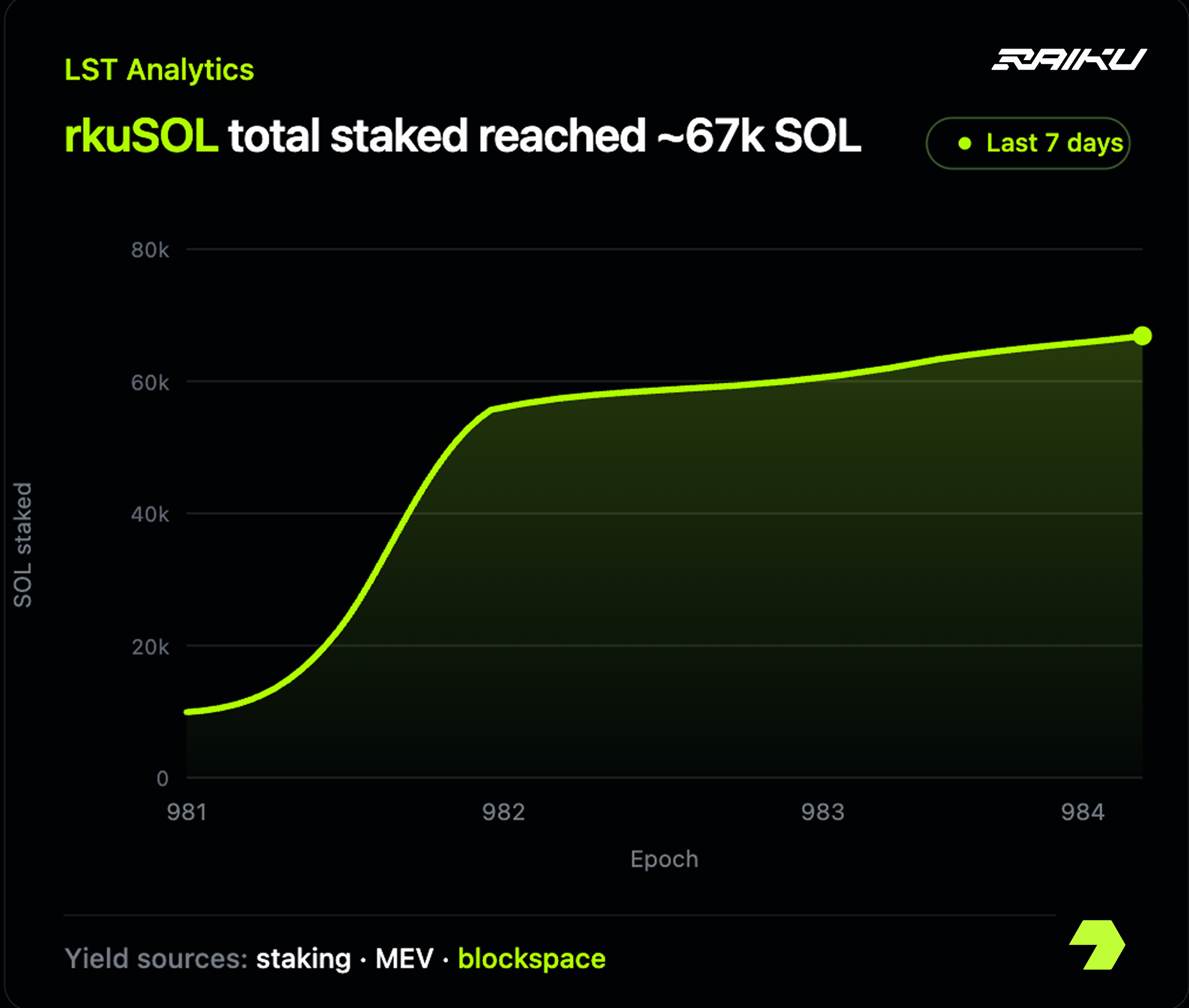

The newest entrant in the top 30, and the only one whose underlying validators earn from a third revenue source on top of staking and MEV. Validators backing rkuSOL sell compute capacity through Raiku's AOT and JIT auctions, both running as first-price sealed-bid, and the revenue flows back to stakers through the same proportional-stake distribution every other LST uses. It's the first material expansion of the Solana LST yield base since MEV arrived, which is the more interesting bit of the launch news than the TVL position. One week in, the product has roughly 67,000 SOL staked and a place in the top 30, with three DeFi partners (Kamino, Loopscale, Exponent) building around the yield curve and the RockawayX rkuSOL vault aggregating exposure across them.

What the picture actually shows

A few observations worth pulling out…

The largest LSTs in the market by TVL are mostly in Group 4. bnSOL sits at the top with more than ten million SOL, almost entirely from exchange-side flows that don't touch Solana's underlying infrastructure, and app-tied LSTs cluster behind it. The work-first LSTs like JitoSOL and dzSOL sit further down the rankings than their actual network impact suggests. There's a real divergence between where TVL flows and where structural contribution sits, and that divergence matters for thinking about where capital is actually deployed versus where it's productively used.

The decentralisation-pressure group is the most thoughtful set of products on the list that nobody talks about much. Marinade, Layer 33, BlazeStake, JPoolSolana, vSOL, and the various smaller-validator-favouring pools are doing real ongoing work to keep the validator set diverse, and they tend to get measured against the wrong metric (headline APY) by most holders. They're worth more attention than they get.

The brand wrapper category is the natural endpoint of LSTs as consumer products. They're convenient, they pay yield, they don't ask anything of the holder. The trade-off is that the holder is not really delegating any decision-making about Solana's future, which is a quiet form of giving up agency. Sanctum dropped the cost of spinning up an LST to nearly zero, and the next year will bring more brand wrappers than ever, which is going to make the question of what differentiates one LST from another increasingly important.

rkuSOL's category, validator-as-multi-product-venue, is the one to watch because it's the first material expansion of the LST yield base in two years. Whether it scales meaningfully depends on how much demand there actually is for the deterministic execution that the underlying validators are selling, but the structural shift in what an LST can be exposed to is real.

What to actually take from this

The top 30 Solana LSTs are not a homogeneous group competing on yield. They're a mix of work-first infrastructure plays, decentralisation-pressure pools, ecosystem builders, exchange convenience products, app loyalty tokens, treasury strategies, and one early example of validator multi-revenue venue economics (which is where rkuSOL sits). Each one is solving for something different, and the headline APY tells you almost nothing about which.

One week in, the rkuSOL product has cleared the threshold of being a real market entrant rather than just another launch announcement. What’s already clear is that both the conditions for the model to scale are in motion. The new yield source is live and starting to compound, three DeFi protocols are actively building leverage against it and the next several months will show how far that trajectory goes.

For anyone reading this who's still thinking about LSTs primarily through the lens of which one pays the most, the more useful question is: what is the LST issuer actually doing with the delegation power that comes with the stake they hold? That's the question this list, and the data behind it, ultimately answers.