The Certainty Economy: Why Solana Needs Guaranteed Execution to Win Institutional Capital

TL;DR: Solana fixed almost everything that kept serious money out, and it still isn't enough. A blockchain guarantees a transaction settles, but not that it lands when you need it, and that gap is a hidden tax retail can ignore and institutions can't. The capital now on Solana won't commit until execution is guaranteed rather than hoped for, and whoever sells that guarantee runs the certainty economy and owns the next era of onchain finance.

Why a high-frequency trading edge doesn't translate to Solana

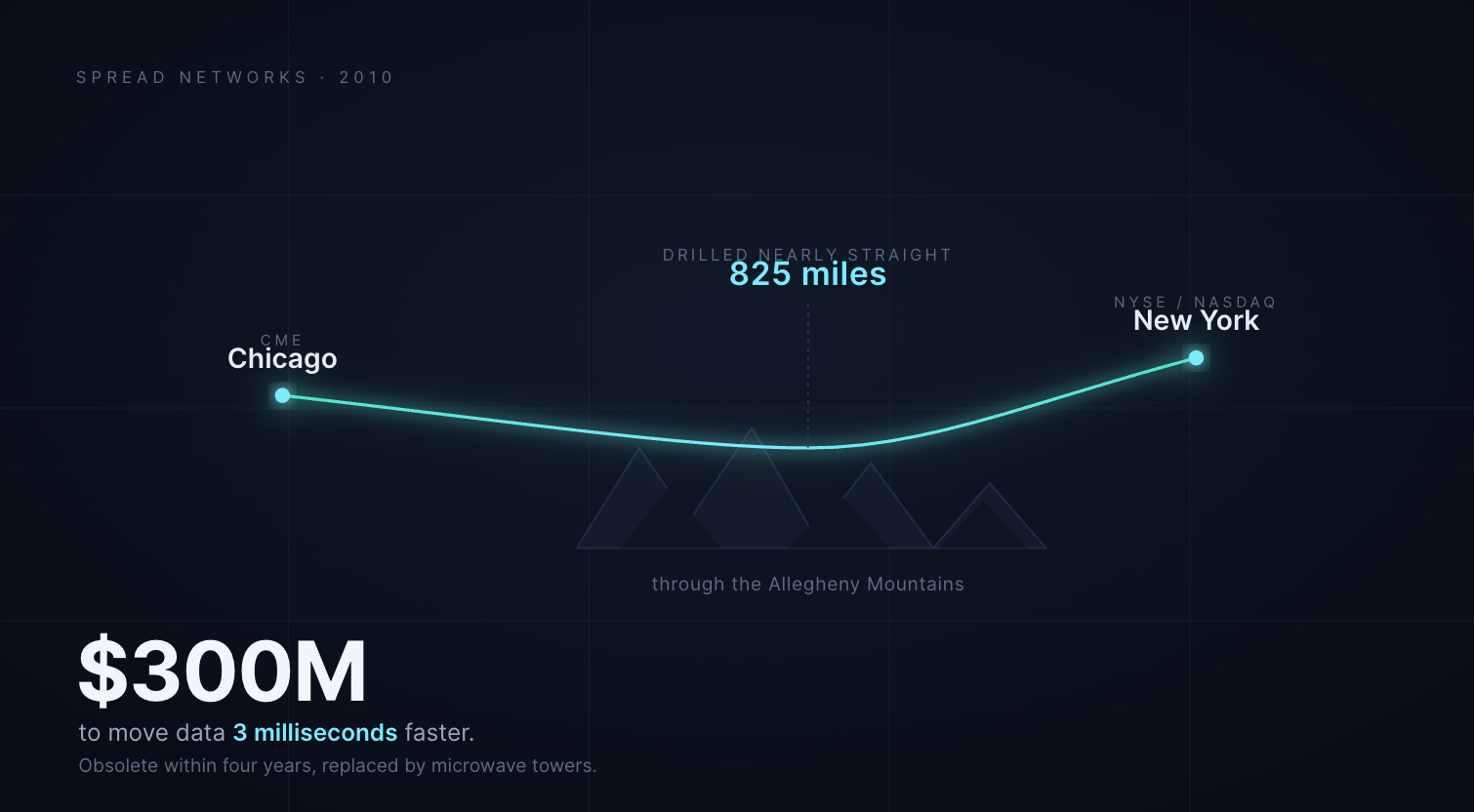

A hedge fund trading on the CME buys its edge with infrastructure. It spends millions to read data and land orders faster than anyone else, renting server space inside the exchange's data center and running the fastest feeds and hardware. In 2010, Spread Networks spent about $300 million laying an 825-mile fiber line through the Allegheny Mountains to move Chicago–New York data three milliseconds faster. None of that buys a trade. It buys a structural edge at one venue, and that edge is a market worth billions.

That edge does not survive the move to Solana. On the CME there is one matching engine, so the only question is how close you can get to it. Solana has no single machine. A couple hundred validators produce blocks at any given moment and the set keeps changing, so there is nowhere to sit close to, and no one can tell you what it would cost to try. For a fund manager that is not an opportunity, it is risk: new fixed costs against unproven returns. So the capital stays where its edge already works.

Settlement vs execution: what a blockchain actually guarantees

Underneath all of it sits a property of public blockchains that rarely gets stated plainly. A blockchain makes one guarantee and quietly withholds another. The guarantee is settlement. Once a transaction lands and finalizes, it is permanent, and the whole network agrees it happened. That part is solved.

What stays uncertain is execution: whether your transaction lands in the block you wanted, in the order you wanted, at the moment you needed it. That gets decided fresh every time, by a competition you re-enter with every submission. It is not a rare edge case either. On Solana, many transactions fail to land during peak demand, the exact moments when landing matters most. So when you press send, you are not buying a confirmed outcome. What you get is a place in line and a probability.

The hidden cost of execution uncertainty on Solana

Uncertainty has always carried a price. The difference onchain is that no invoice ever arrives. You pay in outcomes that come out slightly worse than they should have, and because there is no line item to point at, the cost gets written off as bad luck or the price of doing business. It is neither. It is a fee, and it goes somewhere.

It reaches you through three routes, and they stack on top of each other:

- Slippage and front-running. You submit a swap. Before it settles, a faster actor spots it, buys ahead of you to push the price up, lets you fill at the worse number, then sells into the move you just created. You wanted one price and got a worse one, and the difference became someone else's profit. On a volatile pair inside a busy block, that gap is not a rounding error.

- Failed transactions. Solana charges you even when your transaction never lands. During congestion, as many as 40% of transactions fail to make it into a block, and among high-frequency actors 60 to 90% revert, consuming 35 to 40% of the network's capacity on attempts that accomplish nothing. Each of those failures was paid for. Multiply a small fee by a wallet that trades all day, and the number stops being small.

- Priority fees. When blocks fill up, inclusion turns into an auction. You raise your fee to get picked, the next person raises theirs, and the floor climbs for everyone in the room. Winning that auction still isn't a guarantee, though: a priority fee only raises the probability that the leader includes you, and because it isn't enforced by consensus, your transaction can still be dropped by block-space limits, compute exhaustion, an account lock, or a blockhash that expired before it landed. You are paying for better odds in a line that keeps getting more expensive to stand in, not for the seat.

The cost has a specific shape. You never agree to it, because it is charged the moment you press send. It never reaches you as a bill, so you rarely stop to price it. It flows away from you, toward the fastest actors on the network, rather than to the person actually carrying the risk. Charged without consent, invisible on any statement, collected by someone else. That is a tax in everything but name.

How execution uncertainty hits prop AMMs, perp DEXs, and lending markets

The tax stays abstract until you watch it hit a real operation. The same uncertainty lands differently depending on what you run, and in every case it shows up as money lost or business not done.

The tax stays abstract until you watch it hit a real operation. Two cases show it most clearly, at opposite ends: one that has to fire the instant something happens, and one that has to land at a fixed time.

- Liquidations (perp DEXs). When a position crosses its maintenance margin, the liquidation has to land in the very next slot, and that moment is volatile and congested. Miss it and the position is already underwater, with the loss falling on the protocol as bad debt. In a few milliseconds a position goes from solvent to insolvent, which is exactly the kind of transaction that cannot be left to a probability.

- Institutional settlement. A fund redeeming at a set window, or a tokenized-asset transfer that has to clear on schedule, cannot treat inclusion as a chance. A settlement that misses its window is not slippage, it is a broken obligation, and an institution that cannot guarantee it will not put the operation onchain at all.

The same risk runs through everything else on the network. A market maker whose cancel does not land gets its stale quote picked off and quotes wider to compensate; a lending position that cannot post collateral in time falls undercollateralized; a searcher racing for the next slot pays fees on the 60 to 90% of high-frequency attempts that revert. The transaction that matters is always the one that has to land at a specific moment, and uncertainty is the standing risk that it will not.

Across all of them the pattern is identical. The transaction that matters is the one that has to land at a specific moment, and uncertainty is the standing risk that it will not.

The bill comes due most visibly when the network is under stress. In January 2025, the $TRUMP and $MELANIA token launches drove activity to levels Solana could not clear. People could not complete basic swaps or move liquidity, and many of them were nowhere near those two tokens. The failures were not clumsy users making mistakes. The network was saturated, and everyone standing on it paid at the same moment.

Why execution certainty matters now: institutional capital on Solana

For most of crypto's history, execution uncertainty stayed a background cost because the people paying it couldn't feel it. Retail size absorbs a failed swap as an annoyance and a bit of slippage as a rounding error. That is no longer who is showing up.

Over the past few years, capital from outside crypto has moved onto Solana in a way that is no longer experimental: tokenized equities, stablecoins from issuers like Western Union and a nationally chartered US bank, Visa settling card obligations in USDC, and billions in real-world assets from the likes of BlackRock and Apollo. We covered that shift in full here. What matters now is that this capital behaves differently from the money that came before it, because it measures everything, and it splits into two kinds that need certainty for opposite reasons:

- Fast money (market makers, trading desks) fires thousands of quotes and cancels a day, and it needs to know an order or a cancellation lands in time, because the moment it can't trust that, a faster player picks off its stale quote.

- Slow money (funds, credit and money markets) may send only a handful of transactions a day, and for it certainty has nothing to do with speed. It is about the one transaction that has to work when everything else is going wrong: the redemption, the settlement, the liquidation that cannot fail at the worst possible moment.

Solana spent the last two years fixing the things that kept this capital out, and the fixes are real. Firedancer removed the single-client failure point that outages had made infamous, a token-program rewrite cut transfer costs by around 98%, and Alpenglow is pulling finality from roughly 13 seconds toward the 100 to 150 millisecond range. On SOL-USDC, an onchain trade now costs about 1.22 basis points against 8.33 on Binance's best tier.

But every one of those fixes improves the odds on a transaction rather than making it certain, and better odds are still just odds. The transaction that actually matters cannot run on a probability, whether it is a redemption that has to settle at 4pm, a liquidation that has to fire the second a position breaks, or a cancel that has to land before the market moves. Cheaper, faster, and more reliable still doesn't promise that a specific transaction lands at a specific moment, and until something can, the biggest money stays cautious, for the same reason it has used to weigh every new venue for decades: the returns may be real, but if capturing them means absorbing the risk that the venue fails when it counts, the rational move is to run the math and stay home.

That unpriced risk, the gap between reliable on average and guaranteed for this transaction, is most of what still keeps institutional capital at arm's length, and it is also what a certainty market exists to sell.

How Raiku guarantees execution on Solana: AOT and JIT

Raiku sells that guarantee by changing what your fee buys. A priority fee today buys a better place in line and nothing more, which is why you can pay it in full and still fail when the block fills up. A reservation buys the outcome. Raiku has validators set aside part of their blockspace so you can reserve a slot ahead of time instead of competing for it in the moment. Pay for the slot and the transaction lands, whether you are fast money that needs the next block or slow money that needs a set window. The slippage, the fees on transactions that never landed, the liquidation that fired too late all collapse into one cost you agree to upfront. You stop paying for a chance that your transaction goes through and start paying for the guarantee that it does, which is the one thing an institution can underwrite.

Two products cover the two ways a critical transaction goes wrong:

- Ahead-of-time (AOT) is for scheduled things. A fund settling redemptions at 4pm, or an oracle that has to reprice on time, books its slot in advance, so the transaction lands on schedule even if the chain is jammed.

- Just-in-time (JIT) is for things that can't wait. A liquidation that has to fire the second a position breaks takes the next available slot instead of risking getting dropped under load.

How the auctions and validator commitments work is a separate piece, and that comes next in this series.

Strip away the fiber, the colocation, and the arms race, and what a firm like that spent $300 million on was one thing: the certainty that its transaction would do exactly what it needed, exactly when it needed it. That was the real product all along, and on Solana it is finally for sale directly, reserved and paid for rather than built with hardware or won by being fastest.

That is the certainty economy. Certainty already has a price onchain, paid every day in slippage, missed fills, and liquidations that fired too late. The only question left is who runs the layer that sells the guarantee instead, and that is the ground the next era of onchain finance gets built on.