Solana 2026 Upgrades: What serious finances actually needs and what's now in place

TL;DR: Last week, we walked through every one of Solana's 2025-2026 upgrades and what they mean for everyday users. This piece is the follow-up: what those same upgrades mean for serious finance, the traders, market makers, and institutions moving real size. Onchain execution now beats the major exchanges on Solana's biggest pair, and we break down which upgrades made that possible.

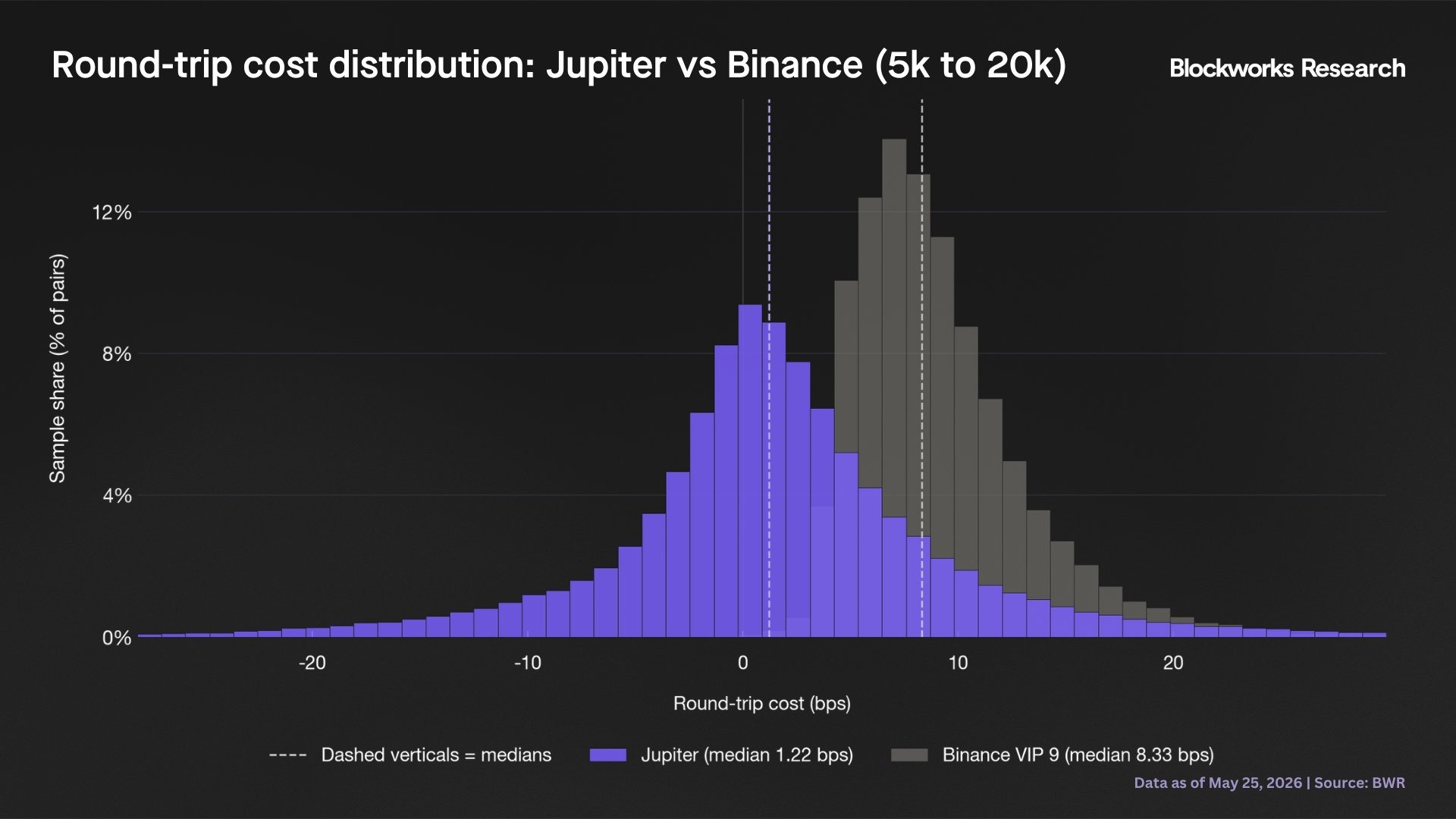

On Solana's most-traded trading pair, onchain execution now beats that of the biggest centralized exchanges. A typical SOL-USDC trade costs about 1.22 basis points onchain versus 8.33 on Binance's best tier, several times cheaper. And for SOL-dollar pairs, onchain volume has now surpassed the combined volume of the top four exchanges.

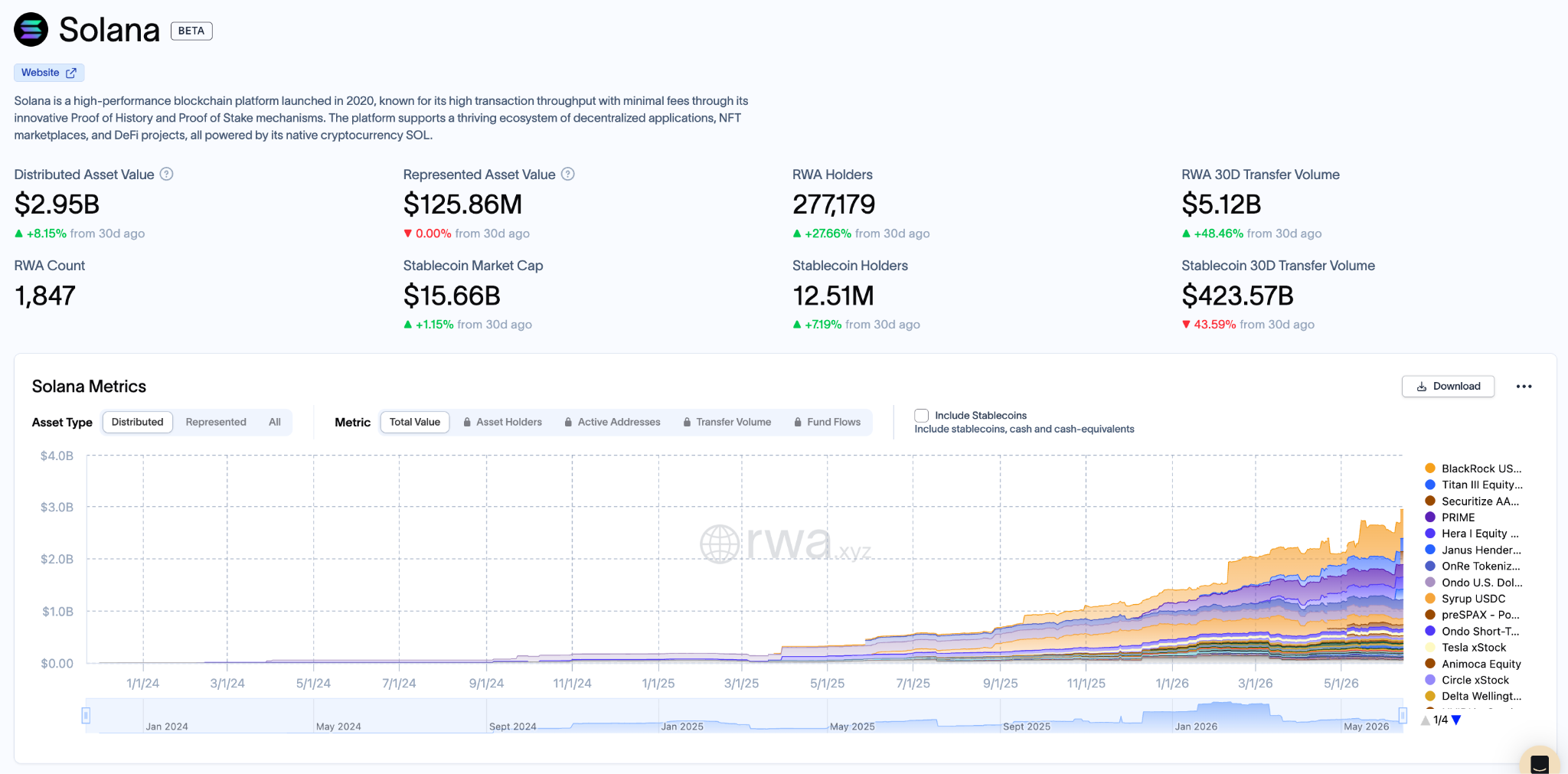

The broader financial stack is moving onchain too. Stablecoin supply on Solana has surpassed $15.6 billion, while tokenized assets have grown to nearly $3 billion, with institutions like BlackRock, Apollo, Janus Henderson, Securitize, and Ondo bringing traditional financial products onchain.

Data source: @Blockworks @rwa_xyz

Put all of this together, and the growth makes sense. These levels of activity and institutional participation weren’t possible two years ago. They didn’t result from any single feature or launch. Instead, they stem from years of steady, incremental infrastructure upgrades that rebuilt the network from the ground up.

That foundation is what now supports the kind of performance serious finance actually requires. By serious finance, we mean the professionals who move real size: market makers quoting prices, trading desks and funds executing large orders, lending and derivatives protocols, and institutions settling tokenized assets. They demand things casual trading never did: execution tight enough for market makers to quote at size, settlement certain enough to strip out counterparty risk, reliability that holds when markets go wild, and costs low enough to operate at scale. A wave of upgrades has been quietly delivering exactly those.

This piece walks through the key upgrades, how they improve these areas, and the remaining gaps.

What serious finance actually demands from Solana

For professional trading operations, the venue is the business. Market makers quoting prices, desks moving size, and institutions settling positions all operate on the same assumption: the network will perform reliably exactly when needed. When that assumption breaks, participants protect themselves by widening spreads, reducing size, routing elsewhere, or avoiding the venue altogether. These defensive actions create thin books and wide spreads, not from a lack of interest, but from infrastructure that cannot be trusted under pressure.

The key risks arise in the short window between deciding to trade and the trade completing:

- Slow settlement: the market can move against you in the gap before a trade is final, leaving you exposed the whole time.

- Laggy or uneven data: if prices arrive late or out of order, you're acting on stale information without knowing it.

- An order or cancellation that doesn't land in time: when the market turns, a faster player can act before you can adjust.

- Congestion mid-volatility: the network slows exactly when you most need to act, the most expensive moment to be stuck.

These issues force wider quotes, smaller positions, and narrower asset coverage. Onchain markets have historically suffered from exactly this dynamic. Each of these demands now maps to specific upgrades on Solana:

- Alpenglow addresses settlement. Reducing finality from roughly 13 seconds to ~150 ms shrinks the open-risk window that forces defensive quoting. (In advanced testing and gradual rollout as of mid-2026.)

- DoubleZero improves data delivery. This dedicated fiber network provides low-latency, low-jitter feeds directly from validators. More reliable and consistent pricing data allows market makers to quote tighter and expand coverage beyond the most liquid assets.

- Firedancer strengthens uptime and resilience. As a high-performance C++ validator client running in parallel with the existing client, it reduces single-client risk and helps maintain performance during spikes, directly addressing past outage concerns that kept some institutions on the sidelines.

- Capacity and cost improvements (including larger blocks, the optimized p-token program, and local fee markets) handle volume and economics. These changes provide more block space overall, lower per-transaction costs, and prevent congestion in one area from raising fees across the entire network. Market makers can now run high volumes of quotes and cancels efficiently.

- Constellation targets ordering fairness. Still in the proposal stage, this multiple concurrent proposers design aims to make transaction inclusion and sequencing more neutral and predictable, reducing the risk of selective exclusion or reordering.

These upgrades do not create markets on their own. They solve core infrastructure problems, fast settlement, reliable data, strong uptime, efficient costs, and fair ordering, so that applications and participants (venues, routers, prop AMMs, and market makers) can build effectively on top. Once those foundations are in place, professionals can quote tighter, hold larger size, and cover more assets. That is ultimately what delivers better prices and deeper liquidity for everyone.

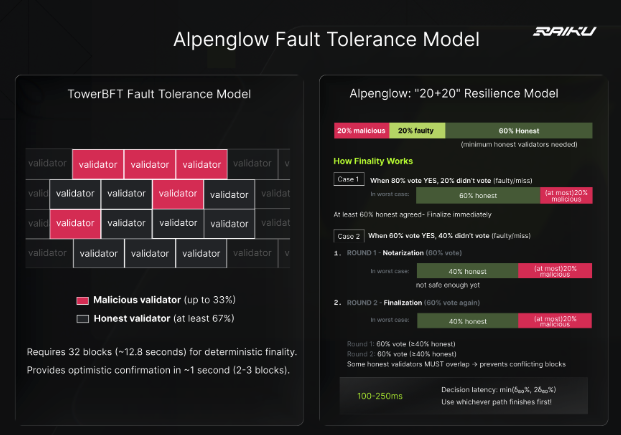

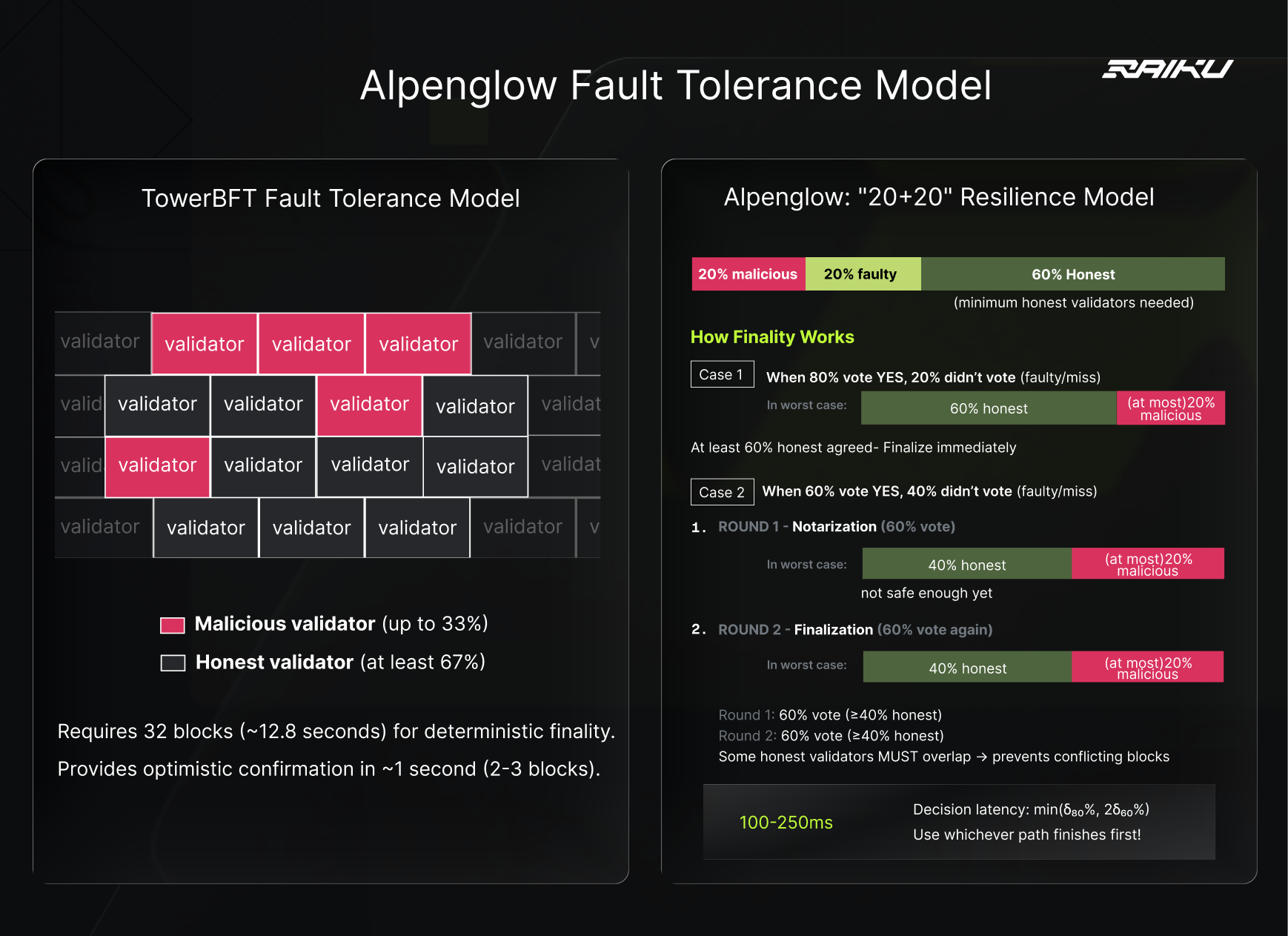

1. Settlement: Alpenglow

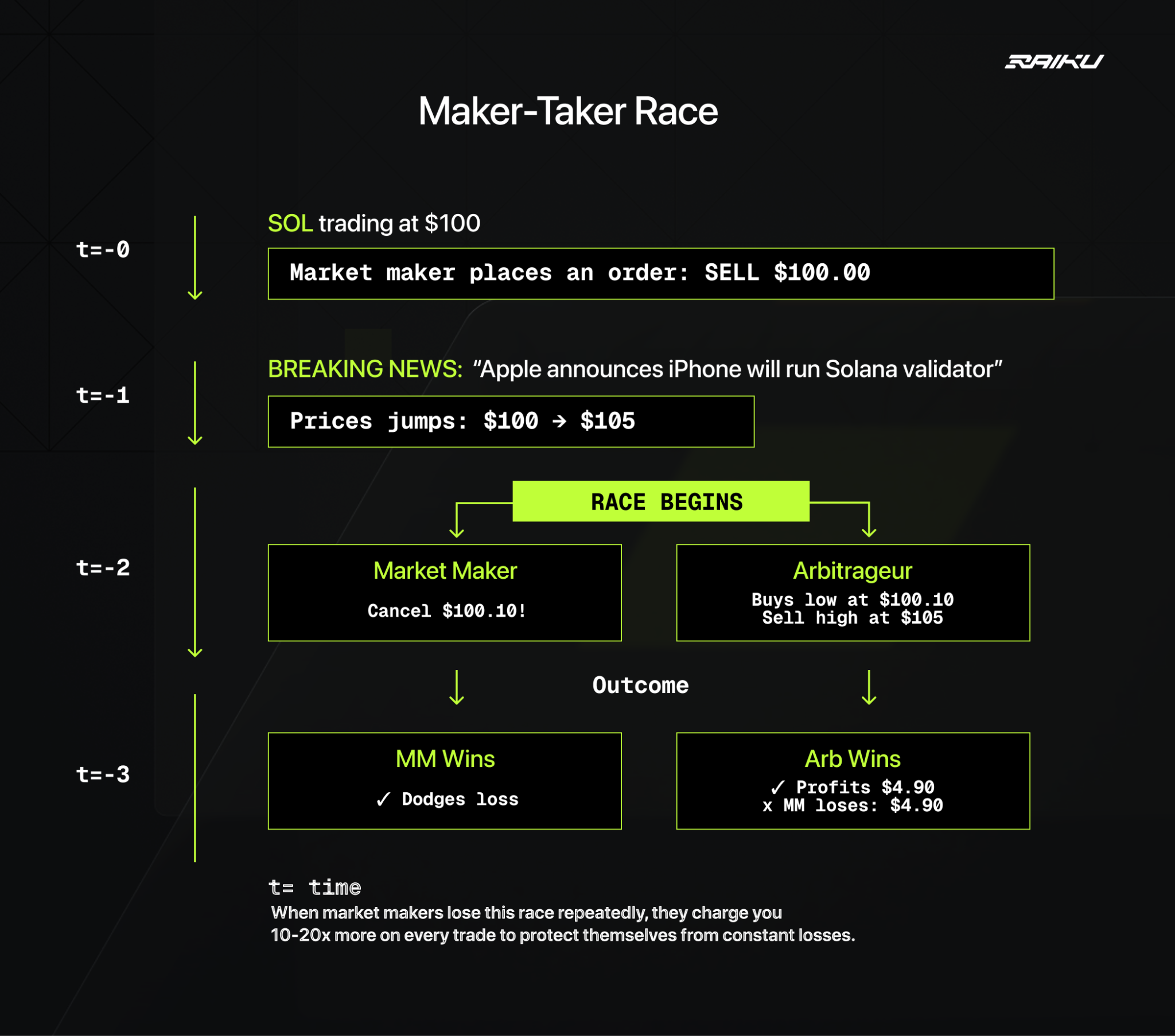

Alpenglow is a redesign of Solana's consensus mechanism that reduces settlement finality from roughly 12.8 seconds to 100–150 milliseconds. For serious finance, that matters because settlement risk is one of the largest remaining uncertainties in on-chain trading, and market makers price every uncertainty they carry into their quotes.

On Solana today, full finality takes roughly 12.8 seconds. During this window, a trade has executed on-chain but is not yet irreversibly settled. The market price can still move against the maker who provided the quote, and that risk shows up as wider spreads, since makers hold extra cushion to protect against adverse moves while they wait for finality.

By collapsing that window to around 150 milliseconds, Alpenglow shrinks the open-risk window dramatically. For prop AMMs and professional market makers, the impact is concrete:

- Tighter spreads on existing pairs: less settlement risk means makers need less premium to cover adverse selection during the finality window. This is already visible in SOL-USDC, where prop AMMs are competitive with or better than major CEXs. Faster finality gives them more room to quote tighter without taking on more risk.

- Deeper liquidity at larger sizes: at bigger clip sizes, the long finality window forces makers to be defensive. Shorter finality reduces the time their capital is exposed, making it more attractive to warehouse larger positions and provide deeper top-of-book liquidity.

- More pairs and lower-liquidity assets: the biggest constraint on breadth isn't just capital or pricing models, it's the cost of defending stale quotes. Faster finality lowers that risk, making it viable to quote continuously across a wider range of assets (BTC, ETH, DeFi tokens, and thinner names) where flow is less balanced.

Alpenglow isn't a standalone fix. It's one part of a broader set of upgrades that together reduce the risk premium makers charge, letting them quote tighter, hold more size, and cover more assets by removing key reasons they currently widen spreads or limit depth.

2. Data: DoubleZero brings predictable data and more assets to quote

Doublezero is a dedicated global fiber network built specifically for blockchains like Solana, replacing the public internet that validators normally rely on with controlled, private paths. For trading, that matters because the public internet is inconsistent, and inconsistent data is something market makers have to pay for.

Validators normally talk to each other over the public internet. For most things that's fine, but for trading it's a problem: data doesn't arrive at a steady pace. Sometimes it's fast, sometimes it lags, sometimes packets drop and have to be resent. That unevenness is called jitter, and it's the enemy here, not raw speed.

A market maker can work with data that always takes 50 milliseconds. What they can't work with is data that goes from 10 one moment to 90 the next, because they can't plan around it. When the feed is unpredictable, a maker may be quoting on stale information without realizing it, and the rational response is to widen quotes to cover the risk or skip an asset entirely. Unpredictable data is a cost, paid in worse prices and fewer markets.

DoubleZero attacks that directly. By routing traffic over private paths, filtering spam at the edge, and distributing updates more efficiently, it delivers much more predictable, low-jitter data. The advantage grows during congestion: the improvement is significantly larger when the public internet is under stress.

This predictability is what matters for makers. When they can rely on consistent, fresh data, they don't need to add as much cushion to their quotes. As Andrew McConnell , CTO of DoubleZero, explained:

"Traditional finance has spent decades building infrastructure where speed and deterministic performance are a real competitive advantage. Onchain markets didn't get that foundation… Deterministic infrastructure removes a risk market makers have to price in, which leads to tighter spreads and better execution."

This has two main effects:

- Tighter quoting on liquid pairs, since makers face less uncertainty from stale data.

- Broader coverage across more assets. Many thinner markets are avoided today because the risk of quoting on stale data is too high. More reliable data lowers that barrier, making it viable to quote a wider range of assets.

One limitation remains: DoubleZero improves data quality and reduces jitter, but it doesn't solve the ordering problem. A maker's update can still be delayed or reordered once it reaches the chain. That sits with other parts of the infrastructure stack.

3. Room and Cost: Bigger Blocks, p-token, and Local Fee Markets

High-frequency and institutional activity onchain doesn’t run on occasional transactions. Market makers send thousands of quotes and cancels every day, while protocols and institutions execute multi-step operations involving transfers, settlements, and liquidations. For this kind of usage to be viable, the network needs three things at once: enough capacity to handle volume without breaking, low enough costs to make constant activity economical, and stable costs that don’t spike because of unrelated activity elsewhere.

Capacity

Solana has steadily increased how much each block can process. Block limits have moved from 50 million compute units to 60 million, with plans to reach 100 million. The goal is simple: give the network enough headroom so that sudden spikes in activity don’t cause widespread transaction failures or sharp fee increases.

The real-world test came on October 10, 2025, the largest single-day liquidation event in crypto history, with over $19 billion liquidated across the industry. This triggered a massive surge in transaction volume. Despite the chaos, Solana remained exceptionally stable: average slot duration only rose from 392 ms to 395 ms, and the block skip rate actually improved to 0.05% (versus a 0.47% baseline). The increased block capacity played a key role in preventing congestion. Underpinning this is XDP, a networking upgrade that enables validators to efficiently process the much larger data volumes of larger blocks.

Transaction Efficiency

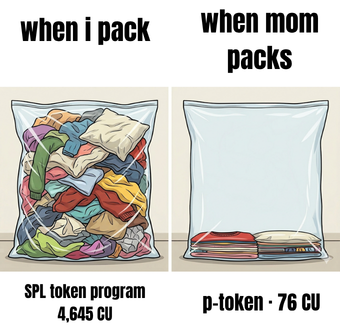

Another way to create more room is to reduce how much compute each transaction consumes. The most impactful change came from rewriting Solana’s core token program. The new p-token implementation cut the compute cost of a basic token transfer by roughly 98%. Because almost every financial action on Solana, swaps, settlements, liquidations, and distributions, ultimately involves moving tokens, this optimization made complex, multi-step transactions significantly cheaper across the board.

At launch, the change immediately freed up more than 10% of total block space network-wide, without requiring any application to update its code. Similar efficiency improvements were made to token account operations and transaction memos, which are commonly used for compliance and payment references.

Cost Stability

Low average fees are not enough for serious participants. What matters is predictability. On most blockchains, congestion anywhere in the network drives up fees for everyone. Solana uses local fee markets instead, meaning congestion is priced at the account level. A spike in activity on one token or pool only raises fees for transactions that touch that specific state. All other activity on the network remains unaffected.

This separation was clearly visible during a major token launch, when intense activity on that single token pushed the network’s average fee up to 41 cents, while the median fee stayed at a fraction of a cent. For institutions moving stablecoins or settling tokenized assets, this matters: their costs remain stable even when other parts of the ecosystem experience extreme demand.

These upgrades don’t directly improve spreads or execution quality on their own. What they do is create the basic operating conditions, sufficient capacity, low costs, and cost predictability, that allow professional market making and institutional flows to function at scale on-chain without constant friction.

4. Fair ordering: Constellation

Every upgrade so far has removed a mechanical risk, slow settlement, jittery data, unreliable uptime, or unpredictable costs. Constellation tackles something different: fairness in transaction ordering. It’s also the least mature of the major upgrades.

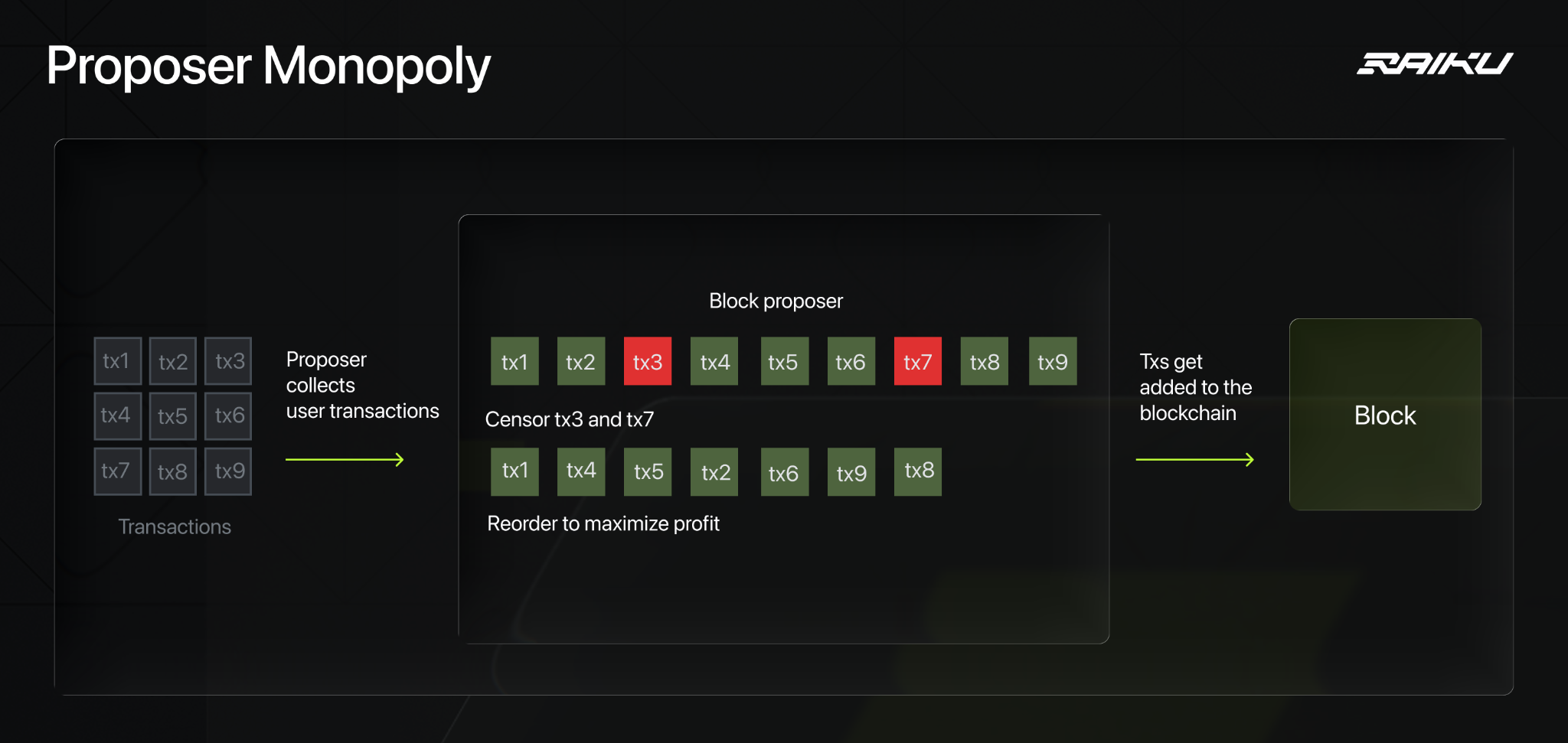

The problem: On Solana today, a single validator becomes the leader for each block and has full control over which transactions get included and in what order. Because there’s no public mempool, the leader sees incoming transactions before anyone else. This gives it the power to:

- Reorder transactions to its advantage

- Front-run or sandwich large trades

- Delay or drop transactions it doesn’t like

This is the root of much on-chain MEV. For market makers, the risk is clear: if they can’t trust that their cancel will land before someone picks off a stale quote, or that their order won’t be quietly reordered against them, they widen spreads or simply avoid quoting certain assets. Many professional traders have cited this lack of reliable ordering as one of the biggest reasons they still hesitate with Solana.

The fix, part one: Multiple Concurrent Proposers (MCP). Constellation breaks the single-leader monopoly by not having a single builder:

- Around 16 proposers operate at once, each independently collecting transactions.

- A separate set of attesters cryptographically signs off on what those proposers received, creating a tamper-proof record of which transactions were seen.

- That record binds the final builder: if a fee-competitive transaction was attested by enough of them, the builder must include it, or the block is invalid and the network rejects it.

The result is a hard inclusion guarantee. Quietly excluding a fair-priced order stops being merely discouraged and becomes cryptographically impossible, because no single validator has the power to do it anymore. In trading terms, that begins to remove the leader-monopoly premium, the cushion makers add to protect against a leader exploiting its position.

The fix, part two: Application-Controlled Execution (ACE). MCP fixes who controls the block, but different venues need different ordering rules. A perps exchange wants maker cancels processed before incoming takers; a lending protocol wants a collateral top-up processed before a liquidation fires. ACE lets an application define its own ordering rules and have them enforced at the protocol level. MCP gives the fair playing field; ACE lets each application set fair rules for its own game on top. Together they're what it would take to match the controlled execution specialized chains like Hyperliquid built, without giving up Solana's openness.

The shortcomings:

- It doesn't stop front-running. A proposer still sees a transaction before it's finalized and can act on it, so sandwiching isn't solved. Worse, submitting to several proposers for a stronger inclusion guarantee exposes the transaction to more parties, widening the attack surface rather than narrowing it.

- Timing games can't be punished. A proposer can delay forwarding a competitor's transaction just enough to push it out of the window. It's indistinguishable from ordinary network lag, leaves no proof, and the proposal itself admits it can't be penalized. This is the largest open gap.

- It doesn't fix concentration. Proposers are chosen by stake weight, so the same large validators dominate. Sixteen is better than one, but it isn't decentralization, and one operator running many validators could hold several slots.

- It costs some speed, and that's contested. The extra coordination adds latency to execution. It increases the time to execute but decreases the uncertainty of whether a fair order lands at all, and which matters more is actively debated.

- It isn't live. Constellation is still a proposal, depends on Alpenglow shipping first, and leaves core details to a later specification. There are no real-world benchmarks yet.

The honest read: MCP plus ACE would solve the most blatant unfairness, a single validator quietly censoring or burying your order, by making it impossible by design and letting each application enforce its own ordering rules. That's a real foundation for trustworthy markets. But it doesn't stop front-running, can't punish timing tricks, leaves today's big validators dominant, and remains a proposal rather than a shipped feature. A genuine step toward fair markets, not the finish line.

5. Uptime under stress: Firedancer

A network that goes down is worse than one with wide spreads. You can quote around a bad price, but you can't hedge, adjust, or run liquidations when the chain stops, and outages tend to hit at the worst time, during high volatility and heavy volume.

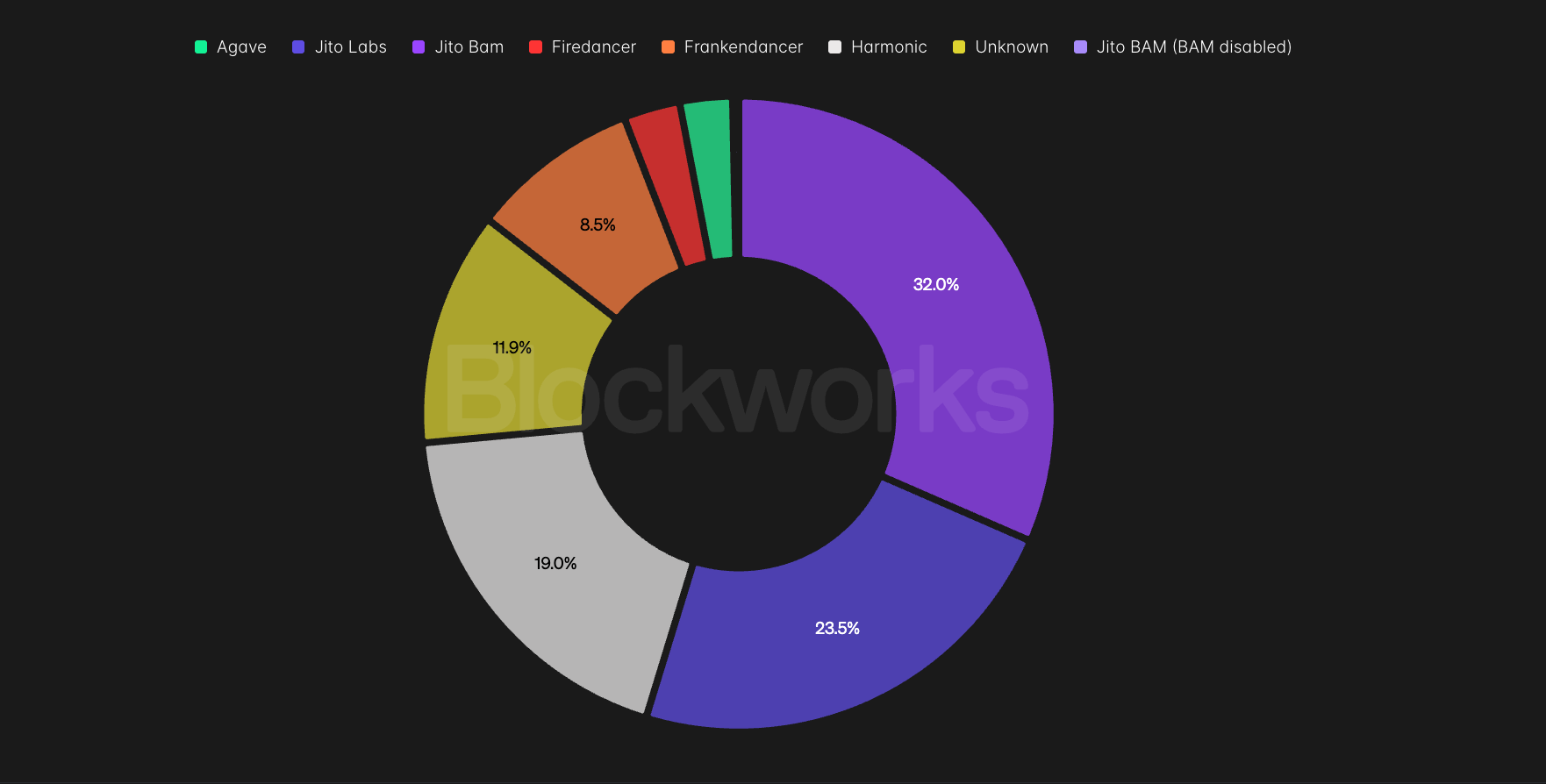

For years, Solana's biggest risk was client concentration: the vast majority of stake ran on one validator client (Agave) and its forks, so a single bug could threaten the whole network at once, as it previously did. Institutions named this as a top reason they kept serious capital on the sidelines.

Firedancer fixes this with a fully independent second client, built from scratch by Jump Crypto in C, sharing virtually no code with the original Rust client. A bug in one no longer risks taking down the other, and its modular design isolates faults within a single validator too.

Live on mainnet since late 2025, Firedancer and its hybrid Frankendancer have produced tens of millions of blocks with zero consensus divergence. Adoption is still early though: standalone Firedancer is a low single-digit share of blocks, with Frankendancer adding several percent more, while the Agave and Jito families still produce the large majority. Single-client risk is meaningfully reduced, not eliminated, but a second independent client is what finally removes the failure point institutions pointed to for years.

Conclusion: the foundation is ready, the building is underway

It's worth being precise about what all this does and doesn't prove. The upgrades built the foundation that a serious market needs: fast settlement, reliable data, uptime, low cost, and fairer ordering on the way. They did not, on their own, build the markets. That work belongs to the application layer, the venues, routers, prop AMMs, and market makers that actually quote prices. And the proof it's working is already visible, with on-chain execution on SOL-USDC matching or beating the largest exchanges.

Where the foundation is ready, but the building isn't, the gaps are real:

- Price discovery still happens elsewhere. On-chain markets today mostly execute around prices set on Binance and other centralized venues. Solana is becoming the best place to fill a trade, not yet the place where the price is made. Closing that gap needs on-chain order books and venue designs that are still early.

- Depth at size lags. On-chain execution wins at normal trade sizes but still loses to the major exchanges on large blocks, where books are thinner, and makers quote defensively.

- Perps remain the clearest unfinished market. Perpetual futures are the largest market in crypto, and Solana is losing it badly, with Hyperliquid doing many times the combined volume of all Solana perps venues. The infrastructure has improved, but the products and retail flow haven't kept pace. Better infrastructure is necessary, not sufficient.

The network was rebuilt into something professionals can finally trust, and serious finance has started to show up as a result. But infrastructure clears the ground; it doesn't fill it. Whether Solana becomes where the world's markets are made, rather than just mirrored, depends on what gets built on its solid foundation now.