The $20B Question: When Perps?

Perpetual futures are the dominant derivatives product in crypto. The instrument is now expanding into equities, commodities, and FX through onchain venues, 24/7, stablecoin-settled, with leverage traditional brokers don't offer. Whichever chain hosts this market at scale captures the single most valuable category in onchain finance.

Solana was built to be that chain. 6 years after mainnet, spot trading works, onchain spreads match centralized venues on most major pairs. Perps don't. Hyperliquid runs 5-10x the volume of every Solana perps venue combined, and the gap has only widened.

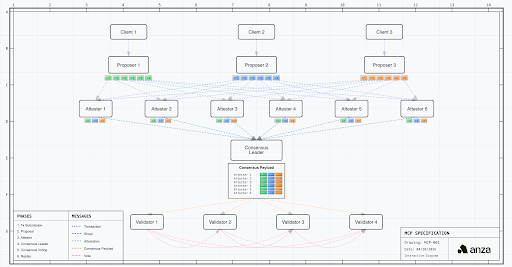

On March 25th, Anza proposed Constellation, the first formal protocol-level design for Multiple Concurrent Proposers on a production blockchain. For perps, this is the first real attempt at giving onchain venues the execution guarantees they need, cancels that land on a known timeline, ordering that doesn't change every 1.6 seconds, and inclusion latency bounded at 50ms. The single-leader monopoly that has been the core reason market makers quote wider on Solana than on Hyperliquid goes away.

Ordering isn't the only thing holding perps back though. Spot markets already hit single-digit-bp fills under the same ordering conditions, and application-level sequencing (ACE) could give perps venues the custom ordering rules they actually need without waiting for a full MCP redesign. On top of ordering, the fee stack, backend systems, product quality, and retail conversion all sit as layers no protocol upgrade touches. MCP addresses the foundation. Other layers still need builders.

On ordering, Constellation picks Frequent Batch Auctions over First Come First Served. FCFS is what every major traditional exchange runs on and what market makers instinctively prefer, but it can't be enforced on a decentralized network without a global clock. FBA at 50ms windows is where MostlyData_'s research shows batch auctions start to earn their place over continuous ordering.

Real tradeoffs remain. Added latency at some pipeline stages, disputed bandwidth impact, and a new extraction surface when the same validator ends up as both proposer and leader in the same cycle, which happens often for high-stake operators. Anza has acknowledged these openly rather than hand-waving past them.

Constellation is entering SIMD governance now. Whether it ships as proposed, gets modified through community debate, or loses to a simpler alternative will decide whether Solana closes the perps gap in the next twelve months, or watches Hyperliquid compound further.

Part 1: Solana's top priority is solving perps

When Solana launched mainnet in March 2020, the vision was simple: build a chain fast enough and cheap enough that a real orderbook could live onchain at the speed of centralized exchanges. 6 years later, most of the other pieces of that vision were shipped. The orderbook wasn’t.

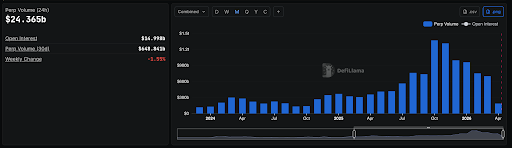

Meanwhile, the market it was supposed to capture has only gotten bigger. Daily perp volume across crypto sits north of $14B, with monthly volumes that crossed $1T at peak and continue running in the hundreds of billions.

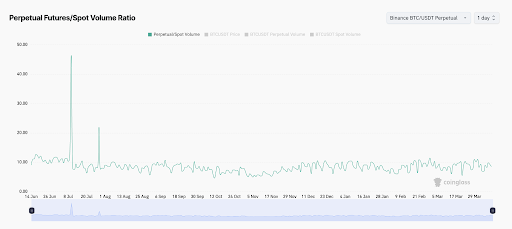

On Binance BTC/USDT, the perp-to-spot ratio holds between 7x and 10x, with occasional spikes higher. Every dollar of spot BTC traded is matched by 7 to 10 dollars of perp volume on the same venue. Perps are also expanding beyond crypto, equities, commodities, FX, all now tradeable 24/7 with leverage traditional brokers won't touch.

Perp DEXs do around $20B in daily volume. Global derivatives (options, futures, CFDs) trade roughly $8T per day. The entire onchain perps category sits at under 1% of that.

Onchain derivatives run on a very different cost base though. A CEX carries banks, custody, compliance, and large teams. A DEX is code running 24/7 that keeps nearly everything it earns. Even capturing a few percent of global derivatives volume at that cost structure produces revenue comparable to the largest traditional exchanges on earth.

Tokenizing spot assets is slow. Every stock and commodity needs custodians, legal structure, and regulatory wrappers. Perps cut all of that out. A synthetic contract tracking a price doesn't need anyone holding the underlying collateral, it just needs a venue good enough to trade it. If Solana wants to host the world's markets, perps are the only realistic path to getting there at speed.

Part 2: Why Solana perps are stuck

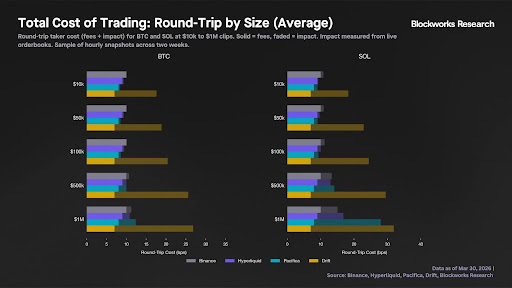

Hyperliquid runs 5-10x the volume of every Solana perps platform combined. Blockworks Research measured round-trip costs (total cost of buying then selling, fees plus market impact) across venues:

Hyperliquid matches Binance at every trade size from $10k to $1M

Pacifica is competitive at small sizes, but it falls apart at scale

Drift costs 2-3x more than anyone else, this gap widens with size

Drift pricing deviates -16 to +10 bps from Binance regularly. Hyperliquid and Pacifica stay within 1-2 bps consistently

Purpose-built chains like Hyperliquid won perps by controlling every layer of execution. This means co-located validators, fixed fees, opinionated sequencing and cancel priority being guaranteed by protocol. Solana made the opposite bet and the properties that make it the most complete ecosystem in crypto are exactly what make perps so hard to build here.

Problem 1: The Ordering Problem

Perps are the most unforgiving product you can build on a blockchain. A swap that lands 200ms late still settles. A lending deposit that takes an extra slot still goes through. Perps have zero tolerance. Liquidations have to fire instantly or the exchange bleeds. Cancels have to land before incoming takers or makers get picked off. Oracle updates have to execute before positions go stale.

Solana's ordering environment makes all of this extremely difficult. The chain has no single enforced sequencing rule. Different validators run different scheduler software, some process transactions as they arrive, some batch into windows, some hold everything until the end of slot and reorder to extract fees. Leadership rotates every 1.6 seconds across hundreds of validators. Solana's validator client landscape has fragmented across six or more clients running simultaneously, each with completely different ordering logic.

There is no way to audit which scheduler is running, no way to verify what rules are in effect, and no way to build a consistent quoting strategy around something that is unpredictable.

Blockworks measured effective spreads on Drift across every major block builder. The result was identical regardless of who built the block, same wide spreads on Jito slots, Frankendancer slots, Harmonic slots, all of them.

If the problem was bad validators, spreads would tighten when better builders were in charge. They didn't. Same result every time. The problem isn't who's building the block.

Problem 2: The Fee Stack

Base fees, priority fees, tips, multiple landing services each with different sorting logic. Market makers send hundreds of transactions per hour, cancels, requotes, oracle updates, and can't predict what any of them will cost or whether they'll land in time.

Market making runs on modeling. No predictability on cost means no predictability on profitability means no committed capital. So market makers price every possible bad outcome into their spreads or don't show up at all.

Problem 3: The Backend Problem

Fix microstructure entirely and you still hit this wall. A competitive perps exchange needs a real time margin system able to constantly monitor every position, a matching engine that never misses, and a liquidation system that fires instantly during the exact moments the chain is most congested.

Even simple onchain routers have moved parts offchain just to function reliably. A full-fledged risk engine for managing a perpetual futures exchange is orders of magnitude harder. Bulk Trade built their own parallel execution environment inside a validator sidecar specifically because they saw no viable path to running these systems on Solana mainnet.

PART 3: What MCP is and how it will impact perps

Solana's perps problem has many layers: backend systems, products, retail flow. But the infrastructure layer, the one Anza can fix at the protocol level, starts with one validator controlling every block. Constellation is their answer, and five things change for perps specifically.

1. Censorship resistance becomes enforced

Today a validator can ignore your transaction and simply not include it. There's no protocol mechanism stopping them. Under Constellation, that becomes cryptographically impossible. A transaction attested by enough validators must be included, the leader either puts it in or produces an invalid block the network rejects.

The guarantee is all-or-nothing. Within a given cycle, either every fee-competitive transaction gets included, or none of them do. A leader can't cherry-pick which cancels to drop and which to honor. For perps market makers, this removes the single biggest source of current uncertainty, spreads today are wide partly because nobody can guarantee a cancellation actually lands.

2. The leader's monopoly breaks

16 proposers collect transactions in parallel. The leader still assembles the final block but is constrained by a cryptographic record of what proposers already saw and attested. They can no longer reorder arbitrarily, delay transactions, or hold everything until the end of the slot to extract value. For perps, this kills WaitUpTo behavior at the protocol level, not through economic pressure but through hard timeouts.

3. Inclusion latency gets a hard ceiling

Inclusion latency today is unbounded. A leader can delay your transaction indefinitely and no protocol mechanism stops them, while Constellation puts a hard 50ms ceiling on this. For a market maker sending hundreds of cancels and price updates per hour, the difference between unbounded uncertainty and a guaranteed 50ms window is the difference between quoting defensively and quoting tight.

4. Geographic paths to inclusion multiply

Today your transaction has one path, reach the current leader, wherever they are. Under Constellation, multiple proposers operate simultaneously across the network. The proposer closest to you geographically receives and attests your transaction without routing all the way to a single distant leader. There are multiple independent paths to inclusion instead of one.

5. Off-protocol fees come back onchain

Activity currently flowing through Jito, landing services, and off-chain fee arrangements returns to the protocol. Two clean fees replace the opaque stack, an inclusion fee and an ordering fee. Under Constellation, competition becomes simple: if you and another trader submit inside the same batch and you pay one lamport more in priority fee, you go first, even if their transaction technically arrived a few milliseconds earlier.

For perps market makers, this matters directly. Predictable costs mean modelable profitability. Modelable profitability means committed capital.

PART 4: FBA vs FCFS in MCP

Changing who controls block construction is one half of what Constellation does. The other half is deciding how transactions get ordered once they reach a block, and for perps this half matters just as much.

Ordering is the rule that decides which transaction goes first when several arrive at the same time. It determines who wins a race, whose cancel lands in time, and whether a market maker can trust the rules enough to quote tight. Every trading venue in the world, centralized or decentralized, runs on some version of it.

There are two main approaches.

FCFS (First Come First Served): Whoever sends their transaction first gets processed first. It's continuous, real-time, and intuitive. Every major traditional exchange runs on it. NYSE, NASDAQ, Binance — all FCFS. Hyperliquid runs on it too. Market makers instinctively prefer it because a cancel fired fast enough is guaranteed to land before an incoming taker.

FBA (Frequent Batch Auction): Instead of processing transactions one at a time as they arrive, FBA collects everything in a small time window and processes them together, ordered by priority fee. The highest bidder in the window wins, regardless of when they arrived. At 50ms batches this means any transaction submitted within the same window competes purely on fee.

The difference matters because each approach creates different incentives. FCFS rewards speed, the fastest connection to the matching engine wins. FBA rewards willingness to pay, where whoever offers the most gets priority. One creates a race to the fastest cable. The other creates an open auction.

Constellation went with FBA at 50ms windows. Here's why FCFS didn't make it.

Why FCFS lost

FCFS works beautifully on a centralized exchange because there's one server, one clock, one authority deciding the order. Everyone races to that single point and whoever arrives first wins.

On a decentralized network it breaks for three reasons.

No global clock. A transaction hitting Tokyo at 10:00:000 and New York at 10:00:003 has no objectively "first" answer across hundreds of global validators. There's no universal timestamp.

Validators can lie about arrival times without leaving any onchain artifact, and since lying is profitable, some will.

It recreates the TradFi colocation race. FCFS rewards whoever is physically closest to validators, which is the same speed arms race HFT firms have been running for decades, just moved onchain. Trading firms would build datacenters next to validator nodes and the fastest connection would win every time. Exactly the pay-to-win dynamic decentralized networks are supposed to avoid.

FCFS inside MCP requires trusting validators not to cheat. That's not a guarantee the protocol can make.

Why FBA works

FBA collects transactions in a small time window and processes them ordered by priority fee. No global clock needed, validators just need to agree on which window a transaction belongs to. No colocation race, being 3ms faster gives you no advantage if you're inside the same batch. Competition shifts from speed to price. Enforceable across multiple parallel proposers without trusting any single entity.

The market already revealed its preference for priority-fee competition. Jito tips, landing service subscriptions, off-protocol block builder auctions, users are already paying for priority-fee-based ordering, just outside the protocol. MCP pulls that activity back inside, distributes the fees to stakers, and makes the competition transparent instead of opaque.

FBA also produces a useful side effect when proposers are distributed globally. Your transaction reaches the closest proposer, gets attested, and gets included within the batch window — often before competitors have time to observe and react. The race effectively ends at inclusion rather than execution. The Constellation paper calls this probabilistic FIFO. You don't get strict first-come-first-served, but you get something close to it as a property of the network's geographic spread, without any of the problems that pure FCFS introduces.

The baggage is TradFi history. Exchanges tried FBA in the UK, US, Europe, and Taiwan, and lost every time. Even short batch delays caused market makers to widen spreads, and liquidity migrated to continuous venues. The concern is real. The question is whether 50ms is short enough to avoid that fate.

Are 50ms batches tight enough for perps?

@MostlyData_ ran exactly this question: at what batch size does FBA actually make sense over continuous streaming?

At 10ms, 20ms, 25ms or 40ms, streaming still dominates across most trading profiles

Only at 50ms does the balance tip

Even at 50ms, half the profiles remain mixed

50ms is the first batch size where FBA earns its place. Constellation's cycle length isn't arbitrary, it's where the data tips.

Solana's network also already has a built-in ~32ms rhythm from FEC propagation, the time it physically takes for transaction data to travel between validators. At 50ms batches, market makers aren't experiencing meaningful additional delay on top of what the network already has.

One more thing worth noting: the 50ms window isn't locked in. If the community decides 25ms or 32ms is tighter to perps needs, the batch length can be tuned through governance. The cycle length is a parameter, not a core design choice.

Cancels landing within 20-50ms means tight quotes. 100-200ms means wider spreads. Unpredictable cancels means no quotes at all. Whether 50ms is tight enough for perps market makers to commit capital is the question Constellation's benchmarks will answer once it ships.

https://x.com/MostlyData_/status/2042234532707901623?s=20

PART 5: What MCP Doesn't Solve for Perps

MCP is necessary but it isn't sufficient. Before getting into specific tradeoffs, two assumptions baked into the MCP-for-perps case are worth questioning.

The first is that ordering is the core reason perps don't work on Solana. It's a reasonable assumption but not a complete one.

The second is that cancel prioritization is the feature that makes Hyperliquid work. Hyperliquid enforces cancel priority, but most major traditional exchanges, Binance, NYSE, NASDAQ, don't, and they have some of the most reliable landings in the world.

What actually matters is dependable infrastructure and predictable rules, not any single ordering mechanic. Constellation delivers predictability, which is closer to what market makers actually need than any specific priority rule.

With those in mind, here are the specific things MCP doesn't touch.

1. Latency TradeoffUnder MCP, your transaction takes a longer path. It goes to a proposer first, gets attested by other validators, then reaches the leader who actually includes it. Each step takes time. Today with a single leader, it's one step. Under MCP, it's three.

For most users this doesn't matter. For perps market makers, it absolutely does. They cancel and requote hundreds of times per hour. If the extra hops add even 20-30ms of latency, their cancels start landing late, quotes go stale, and they get picked off. That's when spreads widen.

2. Leader-proposer collusion is a new attack surface

Under Constellation, a validator selected as leader will often also be selected as a proposer in the same cycle, especially for high-stake operators, where the math makes this common rather than rare. That combination gives full visibility into transaction flow before execution. The operator can see what's coming in, route informed bids through their own proposer role, and win races they wouldn't otherwise win.

The only real mitigation is making latencies tight enough that pulling this off requires extremely close geographic positioning, essentially infrastructure on the same rack. Whether that holds up under adversarial conditions is an open question.

3. Bandwidth impact

Bandwidth goes up under MCP. How much depends on how you count erasure coding, metadata, transaction sizes, and whether market makers send to multiple proposers for redundancy. For perps this matters because market makers send high-frequency updates. If bandwidth scales badly, venues closer to proposers get execution advantages over ones further away, the same geographic effect MCP is supposed to reduce.

4. Retail flow and product quality are the other half

Solana has the deepest retail base in crypto but that base trades memecoins and spot, not perps. Better execution doesn't turn memecoin traders into perps traders. Products have to convince them, interfaces have to onboard them, marketing has to reach them. And even with perfect ordering, someone still has to build the actual perps venue with a great interface, smart onboarding, novel markets, and reasons to choose Solana over Hyperliquid. dYdX fixed execution perfectly and still collapsed because the product wasn't good enough to retain flow. Infrastructure without distribution is empty infrastructure.

Conclusion

Constellation is the most serious attempt so far to close the perps gap at the protocol level. For the first time, Solana has a concrete design that gives market makers what they've been asking for, cancels that land on a known timeline, ordering that doesn't change every 1.6 seconds, and fees that flow back into the protocol instead of out to third-party services. These are real wins, and no other general-purpose chain has delivered them at this scale.

But MCP is one piece of a bigger puzzle. Ordering is only one layer of why perps haven't taken off on Solana. The fee stack, backend systems, product quality, retail conversion, and market maker relationships all sit as separate problems no protocol upgrade touches. And MCP itself isn't the only design being discussed. Shorter slot times, application-controlled execution, and other approaches all live in the conversation, each with their own tradeoffs around complexity and attack surface.

Every month the debate continues, Hyperliquid compounds its lead. Volume attracts market makers, tighter spreads attract more volume, and the flywheel is already running at full speed. Whatever Solana picks has to ship fast enough that the gap doesn't become impossible to close.

Constellation is entering SIMD governance now. Over the next twelve months it either ships as proposed, gets modified through community debate, or loses to a simpler alternative. Whichever happens, the outcome decides whether Solana finally hosts the most valuable market in onchain finance, or keeps watching it compound somewhere else.