The Certainty Economy

TL;DR

Public blockchains were designed for openness. Anyone can submit, anyone can compete, and that openness is one of their most important properties but it’s also, directly, the source of their most important limitation. When execution is contested by design, it is uncertain by definition. For retail investors that uncertainty is manageable, but for the institutions arriving now it is existential: a missed settlement window is a compliance breach, a late liquidation is a bad debt, and an order that lands after the price moves is a loss that compounds with every repetition.

The market forming around their willingness to pay for guaranteed execution is what I call the Certainty Economy. This essay explains why it is forming now, what execution certainty actually requires in practice, why certainty generates yield rather than just removing cost, and why the line between a blockchain you can trade on and a blockchain you can settle on is the most important infrastructure boundary in crypto today, and one that is already being drawn.

Something is shifting in how sophisticated participants think about blockchain infrastructure, and I want to try to name it precisely. For most of crypto's history, the dominant question was whether public blockchains could work at all. Could they scale? Could they attract liquidity? Could they survive regulatory pressure?

Those questions have not been fully settled, but the direction of travel is clear enough that the most interesting participants have moved on to a different set of questions. Not whether blockchains work, but what they are missing. Not whether institutions will come, but what the infrastructure needs to look like before they can fully commit. The answer I keep arriving at is certainty. Specifically: the certainty that a transaction will execute as intended, at the time it needs to, in the conditions it will face. That sounds like a narrow technical requirement. I think it is actually a market-defining one, and the market forming around it is what I mean by the Certainty Economy.

The Contract Nobody Read

When you build on a public blockchain, you accept a set of structural constraints. They are not written down anywhere, but they are real and consequential. I think of them as the Engineering Contract: the implicit agreement that every participant signs simply by choosing to operate on shared, permissionless infrastructure.

The most important clause of that contract concerns execution. Public blockchains were designed to be open. Anyone can submit a transaction. Anyone can compete for blockspace. That openness is one of their most important properties and also, directly, the source of their most important limitation. When execution is open and contested, it is by definition uncertain. You submit a transaction into a shared queue, competing with every other participant for inclusion in the next block. You might land in the position you intended. You might not. The network does not promise.

For most applications, most of the time, that uncertainty is manageable. A retail investor swapping tokens can absorb a few seconds of delay or an occasional failed transaction without material consequence. The expected cost of uncertainty is low, and the benefit of openness and the ability to participate without permission, outweighs it.

The participants arriving on public blockchains now are not retail investors swapping tokens. They are funds settling redemptions at fixed windows. They are protocols liquidating undercollateralised positions the instant a price crosses a threshold. They are market makers firing thousands of quotes and cancellations every minute, each one time-sensitive. For these participants, the expected cost of uncertainty is not low. It is existential. A liquidation that fires a slot late can mean a bad debt that the protocol absorbs. A settlement that misses its window can mean a compliance breach that the fund cannot absorb. An order that lands after a price has moved is a loss that compounds with every repetition.

When the cost of uncertainty is measurable in dollars and the participants are sophisticated enough to price it, they start paying to remove it. That willingness to pay is what creates the Certainty Economy.

Why This Is Happening Now

The Certainty Economy is not a prediction about where blockchain is going. It is a description of something already in motion. Two forces are driving it simultaneously, and understanding both is important for understanding why the market is forming now rather than earlier.

The first is the professionalisation of demand. The capital entering crypto this cycle is structurally different from the capital that drove previous cycles. BlackRock, Franklin Templeton, Visa, SoFi, and Western Union are not retail speculators. They are institutions with legal obligations, compliance requirements, and fiduciary duties that make unpredictable execution not just inconvenient but operationally impossible. A tokenised Treasury fund cannot tell its investors that redemptions might land or might not, depending on network conditions. A card payment network cannot tell its settlement layer that transactions will probably arrive on time. These institutions have spent decades engineering certainty into their infrastructure. When they come to public blockchains, they bring that requirement with them.

The second force is the maturation of the adversarial layer. Execution uncertainty on public blockchains has never been equally distributed. From the beginning, sophisticated participants have profited from the uncertainty that everyone else was trying to navigate. MEV, frontrunning, sandwich attacks, and arbitrage are all expressions of the same underlying dynamic: when transactions are visible in a shared queue and execution order is contested, the participants who can most effectively exploit that visibility will do so. That layer, what I think of as Fast Money, has been maturing in parallel with the institutional adoption story. The people profiting from your uncertainty are getting more sophisticated, better capitalised, and harder to avoid. The people losing to them are increasingly aware of it.

The separation between best-efforts execution and guaranteed execution is not a new problem. Every mature financial market developed the same answer to it: tiered infrastructure. Retail flow moves through open, competitive channels. Institutional flow moves through reserved ones like colocation facilities with guaranteed latency conditions, block trade desks with guaranteed price and size, prime brokerage channels with execution paths unavailable to participants operating in the open market. The insight was not that one approach was superior. It was that different participants have structurally different certainty requirements, and the same infrastructure cannot serve both well. The question the Certainty Economy is answering is the same question traditional markets answered when they built the second tier. Public blockchains have been operating with one. The market is ready for the other.

The combination of these forces creates the market. Demand is professionalising in a direction that makes execution certainty a prerequisite rather than a preference. The adversarial layer is maturing in a direction that makes the cost of uncertainty more visible and more painful. Both movements push participants toward the same conclusion: certainty is worth paying for, and the infrastructure that provides it is worth building.

What Certainty Actually Means

I want to be precise about this because it is easy to conflate certainty with speed. They are related but distinct, and the distinction matters for understanding what the Certainty Economy actually requires.

Speed is a property of the network. A fast network confirms transactions quickly. Solana confirms transactions in milliseconds. That speed is genuinely useful and genuinely differentiating, and the upgrades that have extended it like Alpenglow cutting finality from 13 seconds to under 150 milliseconds and Firedancer improving resilience under load, are real improvements to the infrastructure. But a fast network with probabilistic execution is still a probabilistic network. You can get confirmation in 150 milliseconds and still have no guarantee that the transaction you submitted was the one that landed, in the position it needed to, at the moment it mattered.

Speed tells you how quickly the network processes transactions. Certainty tells you whether a specific transaction will be processed in a specific way at a specific time. The Certainty Economy is about the second property. What the most important participants need is not faster execution of uncertain outcomes. It’s predictable execution of certain ones.

There are two kinds of certainty that matter in practice, and they correspond to two different failure modes.

The first is scheduled certainty. Some of the most important transactions in institutional finance happen at known, predictable times. A fund settling redemptions at the end of a trading window. An oracle updating collateral prices at a scheduled interval. A payment settling at a contractually specified time. These transactions need to be guaranteed not because they are urgent but because they are committed. The institution that issued the contract has promised that the settlement will happen at that time, and if the infrastructure fails to deliver it, the institution is in breach. For these participants, the requirement is simple: reserve the slot in advance. Know before the moment arrives that the transaction will land. Ahead-of-time reservation is the specific mechanism that addresses this class of certainty.

The second is reactive certainty. Other critical transactions cannot be scheduled in advance because they are triggered by conditions that cannot be predicted. A liquidation that has to fire the instant a position breaks. A market maker that has to cancel a stale quote the moment a price moves. An arbitrage that has to execute before anyone else does. These transactions need certainty of a different kind: not that they were reserved in advance, but that when they have to go, they go, without queuing behind lower-priority activity and without being dropped when the network is under load. Just-in-time execution is the mechanism that addresses this class of certainty.

There is a specific property of reserved execution that matters enormously in practice and is easy to overlook. If conditions shift between the moment you commit your intent and the moment the block lands, the transaction aborts before it touches the ledger, and costs nothing. In an open-queue model, the failure modes are asymmetric in the wrong direction: you either land where you did not intend, absorbing slippage or adverse price movement, or you fail and pay for the attempt anyway. Reserved execution inverts that asymmetry. If the execution parameters hold, the transaction lands exactly as intended. If they shift, it does not land at all. There is no middle outcome. That zero-cost abort is not a minor implementation detail. It is one of the core properties that makes reserved blockspace operationally viable for institutions that cannot afford to execute at conditions they did not approve.

Both mechanisms operate on the same underlying principle: instead of submitting a transaction into the open queue and competing for inclusion, you access blockspace that has been set aside. The validator has reserved it. The slot is yours. The outcome is known before the transaction is submitted. What You Send Is What You Get.

Certainty Has a Yield

There is a third dimension to the Certainty Economy that I think is underappreciated, and it is the one with the most direct implications for how this market develops.

Certainty is not only a cost that institutions pay to remove risk. It is also a source of returns for the infrastructure that provides it. When a validator sets aside blockspace and allows a participant to reserve it ahead of time, that reservation generates revenue that would not exist in a purely open-queue model. The participant pays for the certainty. The validator earns from providing it. The protocol captures the auction revenue.

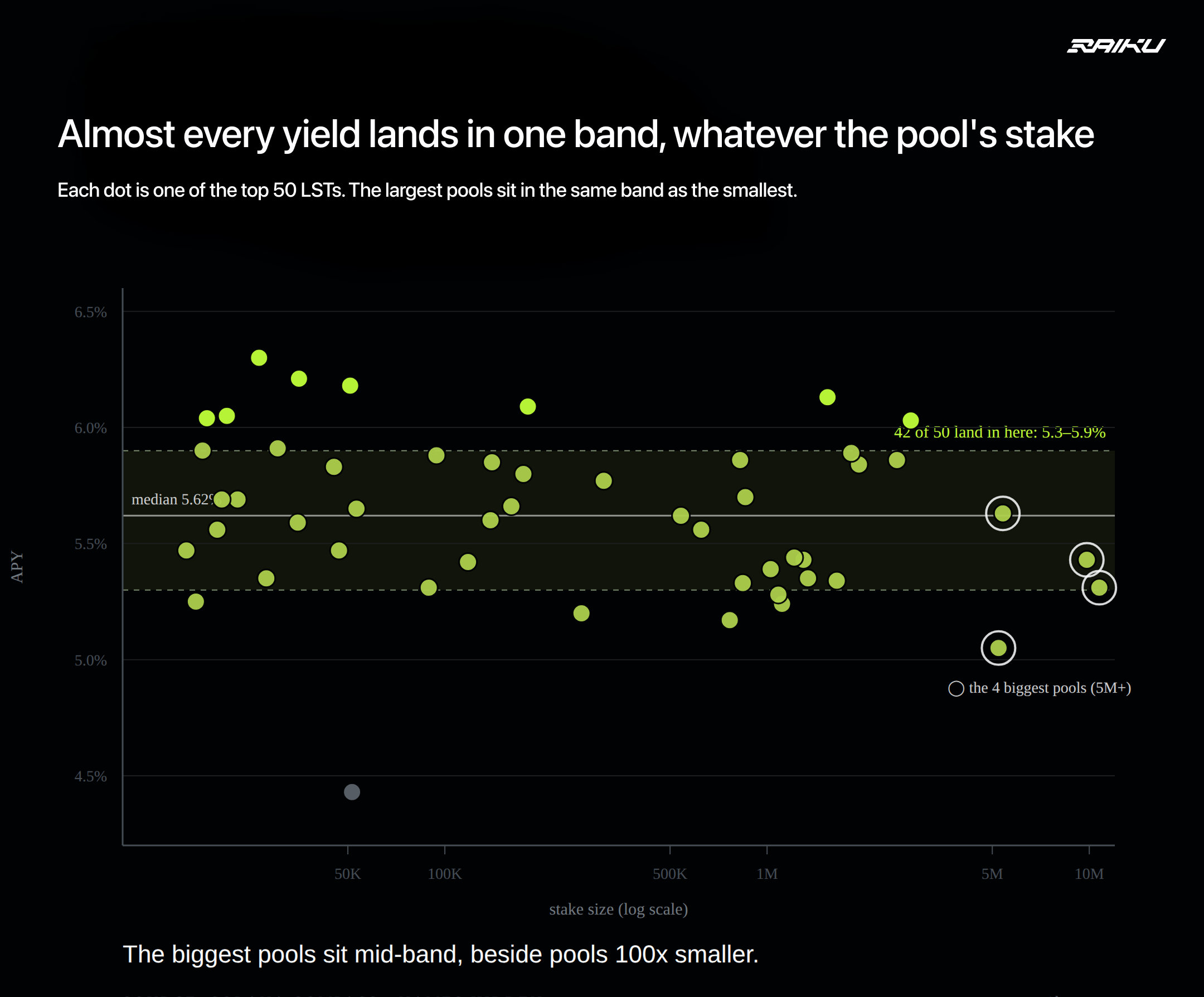

This is the logic behind rkuSOL. Where existing liquid staking tokens pass through two yield streams which are staking rewards and MEV and rkuSOL adds a third: blockspace auction revenue. That third stream exists because Raiku's infrastructure converts blockspace from a contested resource into a reservable one. The certainty that institutions pay for becomes the yield that stakers earn. Certainty has a yield.

This matters for the Certainty Economy argument because it means the market is not purely a cost-of-infrastructure story. It is also a value-creation story. The participants who need certainty pay for it. The validators who provide it earn from it. The protocol that coordinates between them captures the difference. That is a market structure with alignment across all participants, and it is more durable than a market where one party subsidises another.

The Line Between Trading and Settling

The practical consequence of everything above is a distinction I think the industry has not yet made cleanly enough. There is a difference between a blockchain you can trade on and a blockchain you can settle on. Trading requires speed, liquidity, and reasonable reliability. Solana has all three. The $553 million in tokenised equities that traded on Solana on June 25 is evidence of a market that has found a venue it can trade on. Settling requires something more. It requires that a specific transaction, the one that matters, the redemption, the liquidation, the settlement window, lands when it has to. Not probably. Certainly.

There is a structural point embedded in that distinction that goes beyond individual use cases. Solana currently operates as a single-product market: block space, open to all, priced competitively, identical conditions for every participant. That model is what made Solana the fastest and most liquid public blockchain. But it also means that every participant from a retail trader to a fund settling a ten-figure redemption, is buying the same thing and receiving the same terms which are open-queue, competitive and probabilistic. The network will try but it doesn’t promise. The Certainty Economy does not replace that model, instead it extends it. Reserved execution is a different product for a different market vertical, built on the same underlying infrastructure. The validators that provide it earn revenue they cannot earn from open-queue flow. The participants that need it can operate at scale they cannot achieve without it. The capital that committed elsewhere, not for lack of interest in Solana but for lack of a guarantee that matched its operating requirements, now has a product it can actually use. The blockspace market expands because more of the demand that already exists can finally be served. The overall pie gets larger.

The institutions that have arrived on Solana so far have arrived to trade. The ones that will arrive to settle are the next wave, and they are the larger wave. The capital under management at institutions that need settlement-grade infrastructure is measured in trillions, not billions.

The line between trading and settling is drawn by the infrastructure layer that provides execution certainty. That infrastructure is being built now. The Certainty Economy is the market that forms around it.

Why This Argument Starts Now

I have been working through the intellectual architecture of the Certainty Economy across a series of essays, and this piece is the beginning of that series. The reason to start with the Certainty Economy rather than the technical details of how Raiku implements it is that the macro argument has to land before the product logic can be fully understood. The technical story, AOT reservations, JIT execution, blockspace auctions, validator economics, is meaningful only if the reader already understands why execution certainty is the defining infrastructure challenge of the current moment. The product answers a question. The Certainty Economy is the question.

Over the coming months I will work through the deeper architecture of that question: the specific clauses of the Engineering Contract that create the uncertainty in the first place, the long-term trajectory of public blockchains as settlement infrastructure, and the dynamics of the Fast Money layer that profits from the uncertainty everyone else is trying to solve. Each of those pieces builds on this one.

The conclusion is this: guaranteed execution is economically meaningful on public blockchains, the market forming around it is real and growing, and the infrastructure capable of providing that guarantee at scale is the defining build of the current cycle. That is the Certainty Economy and it’s already here.

Robin Nordnes is the CEO and Founder of Raiku, which builds blockspace reservation infrastructure on Solana.